Accounting info. Accounting info How the planned cost is formed in 1s

procedures. How to correctly reflect the costs, what documents to reflect the fact of the release of products (works or services), how the cost is calculated and where given result can see? Let's talk about the nuances of cost accounting and the subsequent calculation of the cost of production in "1C: Accounting 8", ed. 3.0.

Initially, "1C: Accounting 8" is not intended to calculate the actual cost large enterprises with a complex method of accounting and cost allocation. For these purposes, 1C recommends using specialized solutions, such as 1C: Manufacturing Enterprise Management, 1C: Integrated Automation, 1C: ERP. "1C: Accounting 8", ed. 3, allows users to organize and maintain accounting and distribution of costs for small and medium-sized organizations. For the correct and correct calculation of algorithms, it is necessary to take care to reflect the real picture of cost accounting as accurately as possible (by their places of occurrence) and to think over all aspects of the correct distribution of costs by type of activity.

The sequence of calculating the cost of finished products

What in general is the algorithm for calculating the cost of production in "1C: Accounting 8", ed. 3? The mechanism provides the user with the ability to accurately account for materials and semi-finished products previously transferred to production. This feature has been included in the program since release 3.0.53.

A planned, well-coordinated system of accounting for costs associated with the release of products, the provision of services, the performance of work is a prerequisite for a reliable and transparent reflection of information about the activities of the organization in the future. At the same time, when drawing up cost accounting methods, it is necessary to rely on the principles and provisions previously developed and enshrined in regulations on accounting and instructions for calculating the cost of products (works and services) of your organization.

Figure 1 shows how the cost is calculated. finished products in the software product "1C: Accounting 8", ed. 3.

Scheme for calculating the actual cost of production in "1C: Accounting 8", ed. 3.

Correct cost accounting

Let's start with the fact that one of the most common mistakes in calculating the cost is the initially incorrect organization of cost accounting in the context of cost items, places of their occurrence and types of activities. Let's take a look at expense accounts. detailed description how they will be distributed.

The costs of the main and auxiliary production (account 20, 23) will be distributed at the end of the month between the manufactured products and work in progress.

General business and general production expenses are distributed at the end of the month to account 20 (general business expenses can also be distributed to account 90.08 if you select “ By direct costing method”) to a specific site, depending on the distribution base. Variants of all possible bases for the distribution of costs available in "1C: Accounting 8", ed. 3, with explanations are given in table 1.

Table 1. Variants of bases for cost allocation

|

Distribution base |

Description |

|

Planned production cost |

In proportion to the planned cost of manufactured products, services rendered. |

|

Issue volume |

According to the number of products released in the current month or services rendered. |

|

Material costs |

According to the material costs reflected in the items with the type of NU "Material costs". |

|

Selected direct cost items |

In proportion to direct costs, according to cost items indicated in a separate list. |

|

Salary |

According to the cost of wages of the main production workers. |

|

Direct costs |

In proportion to direct costs: for accounting- the costs of the main and auxiliary production, for tax accounting- direct costs of the main and auxiliary production, direct overhead costs. |

|

Distribution occurs in proportion to the proceeds from the sale. |

Cost allocation methods in the program are made in the accounting policy settings (“ Main» – « Accounting policy »).

Indication of methods for allocating indirect costs.

Commercial expenses (account 44) at the end of the month will be debited to account 90.7 “Sales expenses” in proportion to the sales proceeds.

During the reporting period, expenses are recorded in the program by the following documents:

« Invoice claim»;

« Receipt of goods and services» (tab « Services»);

« Advance report» (tab « Other»).

« Reflection of salary in regulated accounting».

The cost at which the inventory is written off to production is calculated in accordance with which option we indicated in the accounting policy:

according to the FIFO method;

according to the average method.

Services rendered by a third party and other non-material costs are included in production costs in the estimate indicated by the user in the document.

Setting up cost calculation in 1C

Now that we have indicated how the correct distribution of costs will occur, we will proceed directly to the calculation of the cost. There are two important things to consider at this step:

the cost is calculated based on item groups;

cost costs are allocated according to the planned cost.

That is, before the calculation, you need to determine the list of item groups and set the planned prices for manufactured products.

Why do we need to specify planned prices? Since the program accounts for manufactured products and services rendered during the month exactly at planned prices, it is only at the end of the month that all costs for item groups are summed up and the real (actual) cost of manufactured products and services is calculated. As you can see, before the closing of the month, we do not have information about the actual cost. However, when generating the document " Production report per shift" And " » setting a price is mandatory. This price is called the planned price. Planned prices are set in the document "1C" " Setting item prices" (Chapter " Stock» – « Prices» – « Price setting»).

Let us now dwell on the nomenclature groups. The 1C:Accounting 8 program calculates the cost exactly by item groups: you can create them yourself, including any item positions in the corresponding item groups. The main purpose of nomenclature groups is to summarize information about products, works, services for homogeneous groups (for example, by type of product, by type of activity).

Documents reflecting production operations

All operations for the release and further sale of products and services are reflected in the following documents:

« Production report per shift» is intended to reflect the output of products and services;

« Provision of production services» is used to reflect the output and sale of production services.

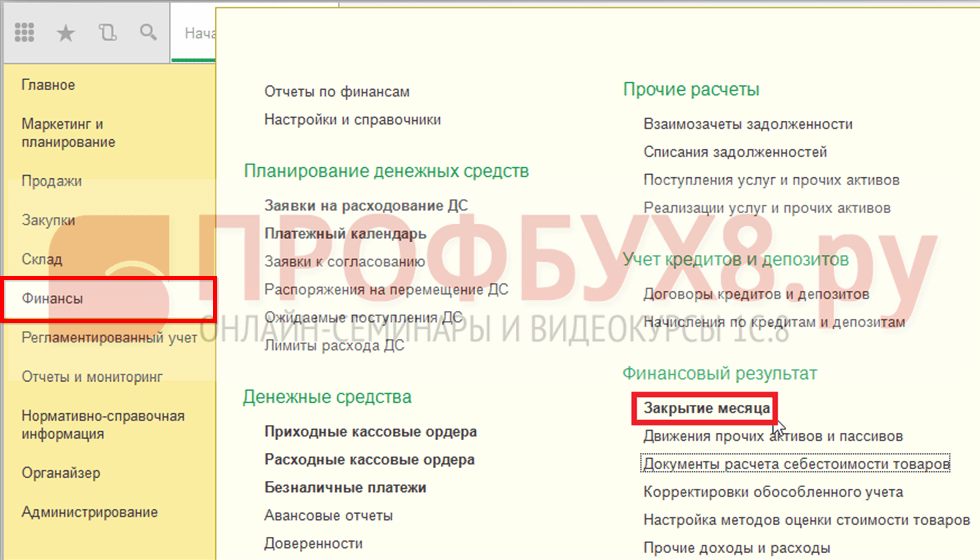

When calculating the actual cost of production (operation " Closing the month”), the planned cost is adjusted to the actual cost with the write-off of deviations. The costs of the main production, not distributed at the end of the period, form the balance of work in progress.

Calculation of the actual cost of products and semi-finished products

And finally, the final step, directly calculating the actual cost. Calculations are performed in several stages:

Direct costs for each product and division are calculated depending on the sequence in which the divisions are closed.

Indirect costs are distributed according to the rules set in the " Methods of allocation of indirect costs of the organization", which was described above.

The calculation of direct costs for each product and each division is carried out according to the sequence of closing divisions, taking into account indirect costs.

Adjustment of the cost of products and semi-finished products from the planned cost to the actual cost.

The absence of errors at the end of the month will indicate the fact that the calculation of the actual cost was carried out according to the rules. You can check the correctness of the calculations using the following reports:

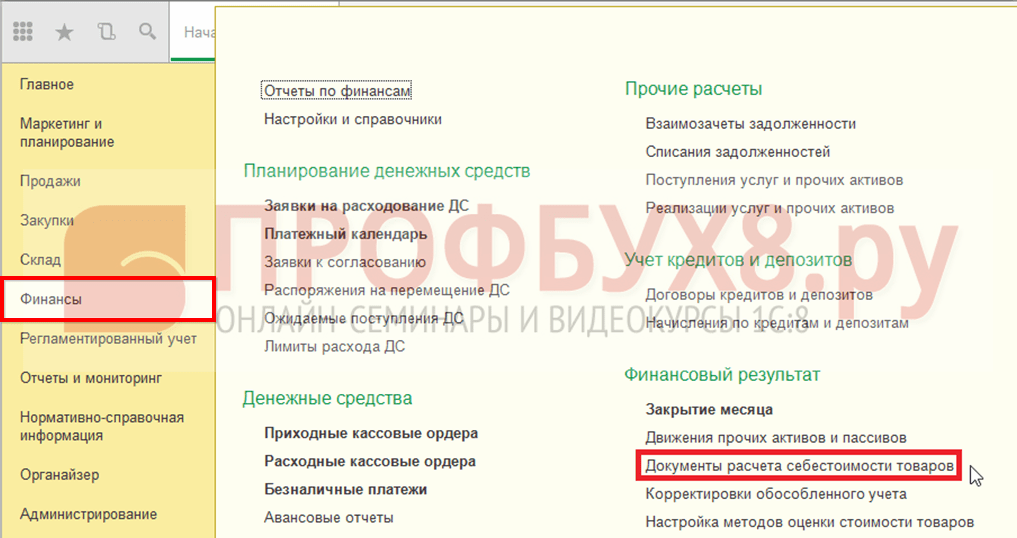

reference-calculation " Costing»;

reference-calculation " Distribution of indirect costs»;

reference-calculation " Production cost».

Standard report "Reference-calculation" Cost of production "

As you can see, the data in the report is reflected in the context of item groups, as described earlier.

If you still notice some inaccuracies, you need to correct the original data and re-calculate the cost.

cost of 1C cost accounting

The choice of the method in accordance with which the calculation of the cost of goods will be performed is indicated in the accounting policy of the organization. To do this, go to the section Regulatory and reference information - Enterprise - Organizations:

The directory of the Organization will open. Here you need to open the necessary organization for editing:

Then you need to go to the Accounting Policy tab:

You can edit an account policy record that has already been created, if it exists. To do this, click on the More button and select the Allow editing details item or create a new one using the Create new link:

The Organization Accounting Policy (Create) window opens. In the Valuation Method field, you must select the required valuation option that will be used when calculating the cost in 1C 8.3 UT 11:

By default, in the 1C 8.3 UT 11.1 program, the Average per month option is set. But you can choose another option from the drop-down list:

You can also set up goods costing methods directly in the Set up goods costing methods lookup, which is not visible on the panel by default. You can open the directory in the section Finance - Financial result by selecting the item Setting up methods for estimating the cost of goods:

Clicking the Create command opens the Customizing methods for estimating the cost of goods (creation) window:

When creating and configuring a directory element, it is possible to set the execution automatic update recalculation of the cost in 1C 8.3 UT 11 when performing a scheduled task. To do this, you need to enable the corresponding option Update cost by scheduled task.

Calculation of the cost price using the document Calculation of the cost price of goods

One of the options for calculating the cost of goods in 1C 8.3 UT 11 is to use the Calculation of the cost of goods document.

In order to open a list of documents of this type, it is necessary in the section Finance - Financial result, select the item Documents for calculating the cost of goods:

By default, in 1C 8.3 UT 11 this command is not visible. To display it on the panel, select the Navigation settings command in the Settings:

The Navigation bar setup form opens:

In the left part of the Available commands form, in the Financial result section, select the Goods costing documents item. Next, by clicking the Add button, we transfer the Selected commands to the right side.

The document Calculation of the cost of goods in 1C 8.3 UT 11 is intended for calculating the cost of goods for a certain period, as well as distributing the total amount of costs for manufactured products. The cost price is calculated from the beginning of the month to the date of creation of the document. Only one document of this type can be entered per month.

In the Documents list for calculating the cost of goods, documents can be created and edited:

Clicking the Create button opens a window of a new document Calculation of the cost of goods (creation):

When you click the Select (...) button in the Organization field, the Select organizations selection form will open:

When posting a document, the cost calculation can be performed in two versions: preliminary and actual:

- When using the preliminary version, the cost data of goods are evaluated online, their average cost is calculated without taking into account additional costs regardless of the method of valuation established as applicable in the entity's accounting policy.

- The actual cost calculation is made at the end of the month. With this method, a predetermined scheme for estimating the cost of goods is applied, and additional costs are automatically allocated to the cost of goods. After the actual calculation, the preliminary calculation data is adjusted:

Cost calculation using Month-end processing

When using the processing Closing of the month in 1C 8.3 UT 11, the cost calculation consists of automatic sequential execution of several operations. After the successful completion of these steps, a document appears containing information on the calculated cost of goods.

Assistant Closing the month in 1C 8.3 UT 11 can be opened in the section Finance - Financial result - Closing the month:

The Scheduled Month-End Closing Operations form opens. The calculation of the cost in 1C 8.3 UT 11 includes the following steps: the formation of movements in batches of goods, the distribution of VAT and the calculation of the cost:

You can perform all operations by clicking the Execute Operations button, or you can perform individual operations by clicking on the desired command in the list.

Calculation of the cost price using a scheduled job

Another option for calculating the cost of goods in 1C 8.3 UT 11 is automatically by performing a scheduled task, according to a configured schedule, or manually.

Get on the list routine tasks you can go to Administration - Support and maintenance:

In the Scheduled operations section, select Scheduled and background jobs:

On the Scheduled tasks tab, select the Cost calculation item, select it and click the Run now button:

An informational message will appear at the bottom of the window:

After the operation is completed, in the End date column, information about the date and time of its completion will appear.

If you double-click on the Cost calculation command, the setup window for this scheduled job will open:

By clicking the Schedule command or from the list of scheduled tasks by clicking the Configure schedule button, you can configure settings for this operation:

To automatically calculate the cost of goods in 1C 8.3 UT 11.1 at the end of each month, you need to go to the Monthly tab, mark all months and in the field Run in set the number 1, and in the field Day of the month select from end:

In the article, we will consider the calculation of the cost of production in 1C using the example of Accounting 8.3. Depending on what the company does, it may be interested in calculating the cost of goods or services. In the general case, we will call "product" both, and the cost will show the amount of the company's costs for production, no matter what exactly is meant by this - the production of goods or the provision of services.

In our calculation, the costs incurred are traditionally divided into direct and indirect. The former usually include the cost of raw materials or some work related directly to the products being manufactured, as well as the salary of employees directly involved in the production process (they are reflected in the accounting of production on account 20).

Expenses related to the entire production site, but not allocated to any specific product group of manufactured products (for example, depreciation costs for the workshop building), are posted to all products manufactured in the workshop in general. Such expenses are displayed on account 25. And here, as part of the accounting policy settings, you can specify different variants such a division, for example, in proportion to the planned cost of production, or the number of units, or apply any other algorithms.

General business expenses are reflected in accounting on account 26 and further, depending on the settings already mentioned, they can be posted to the issue cost in the same way as general production expenses, and also written off using the direct costing method by posting 90.08-26, without being reflected in the issue cost. Very often this method is chosen in the settings.

In tax accounting, direct expenses are reflected in the cost of finished goods and are written off as they are sold, while indirect expenses in NU are written off immediately, at the time of occurrence.

Consider the following example:

The sewing workshop produces two types of products. Skirts and sundresses. The nomenclature groups will be the same.

Skirt specification:

- Fabric 1 m x 500 rubles. = 500 rubles.

- Lace 3 m x 100 rubles. = 300 rubles.

- The planned cost of one skirt is 1000 rubles.

- 150 pieces were produced per month.

Specification for sundress:

- Fabric 2 m x 500 rubles. = 1000 rubles.

- Lace 5 m x 100 rubles. = 500 rubles.

- Buttons 10 pcs x 20 rubles. = 200 rubles.

- The planned cost of a sundress is 2000 rubles.

- 100 pieces produced per month.

In 1C, we write off the price of raw materials / matter according to the specification to account 20.

Additionally, threads were issued to the sewing workshop, which were used for both types of products. We write them off to account 25, and in the settings we set that the threads are posted according to the cost of production at the planned cost.

In addition, depreciation has been accrued for the workshop building, which is also subject to distribution. To show the possibilities of the program, we will establish a method for distributing the depreciation of a building by the number of manufactured products.

In tax accounting, the cost of materials and depreciation will be shown as direct costs.

Settings in 1C for calculation

Setting up the cost calculation begins with the accounting policy, where accounting conditions will be set, and Taxes and reports, where tax features are noted.

Menu path: Main-Settings-Accounting policy / Taxes and reports

The section that affects accounting is shown below. Materials will be written off at average prices, general business expenses using the direct costing method.

In order for the program to be able to determine which expenses for NU are direct, they must be directly specified in the corresponding setting. The remaining costs, if they are not non-operating, will be considered indirect. Let's set that are direct for NU purposes regardless of the account.

You may also need to look at the section Reference books and check or fill in item groups and cost items.

Their filling depends on the accounting features of each enterprise, it is difficult to give a single advice in this case. For the correct operation of 1C, it is necessary to add at least one item group, sometimes it is called that - The main nomenclature group.

If necessary, you can make different details. For example, the atelier sews products to order and is engaged in cutting. Then you can make two groups - Tailoring of products and Provision of services. And you can expand this list and, for example, additionally make detailing according to the nomenclature of garments depending on the type of product. Approximately the same situation with the costs - the degree of detail may be different.

To display the output, go to the section Production. We need a document Production report per shift. If they provided services, they used here

Filling out the tab Products.

Then tab The example uses specifications, so you can use the button Fill to set the quantity automatically. You can also fill in the list of materials manually.

There is a button in the directory of the item being created

We write off the threads with a document

When performing this processing, depreciation on fixed assets was accrued.

It is also possible to correct the cost of the item. For example, if there were several receipts at different prices, and the write-off should occur at the average, then when performing this operation, the average price of the item item will be calculated, then the write-off amounts to production will be adjusted.

The main cost calculation occurs when cost accounts are closed. You can see references-calculations for operations.

We examined the basic capabilities of the 1C Accounting program for accounting for the cost of production. It should be noted that the 1C Accounting configuration is designed for small and medium-sized enterprises with simple production accounting. If it is planned complex production, many redistributions, counter production, etc., it is recommended to consider such 1C configurations as ERP or KA.

Act on the provision of production services). Let's generate the report "Turnover balance sheet for account 20.01": 6. Consider the formation of the cost of services without using planned prices. Let's issue the provision of services for "object 2" with the document "Sales of goods and services": Document postings: The planned cost is not indicated, accordingly, no postings are generated for it. 7. Let's re-carry out the "Closing of the month" with the flag "Calculation and adjustment of the cost of products (services)" set. Let's look at the postings of the document: It is clear from the postings that total cost services for "Object 2" is written off at the end of the month in full.

- With an open date Accounting for payroll.

Accounting for the sale of services in "1s: accounting 8" (rev. 3.0)

Important! It is necessary to observe the correspondence between the write-off of costs and the accounting for the services rendered.

- First, costs and production services must have the same item groups.

- Secondly, production services must be reflected in the document "Provision of production services" (or "Act on the provision ... in the old version"). When using the document "Sales of goods and services", cost accounts will not be closed, cost adjustment will not be calculated (no allocation base!)

How to check the production cost? In conclusion, we give examples of reports that appeared in the latest editions of 1C 8.3 Accounting: Help-calculation of the cost of products manufactured, services rendered: Help-calculation of costing: These reports are generated after all routine operations have been completed and can be called directly from the processing form “Closing the month ".

Provision of production services in 1s 8.3 accounting 3.0

Enterprises 8 edition 3.0. provided various ways their reflections. So, depending on the methodology for accounting for operations for the sale of services and the methods for forming the cost of services rendered in 1C Accounting Enterprise edition 3.0, services are divided into:

- production services (for which the planned cost is determined);

- services for the manufacture of products from customer-supplied raw materials;

- other services, the costs for the provision of which are charged to account 20 "Main production";

- services related to trading activities;

- other services (the costs of which are charged to accounts 26 “General business expenses” or 44.02 “Commercial expenses in organizations engaged in industrial and other production activities”.

In this article, I want to consider two ways to reflect the operation of the implementation of services - the most common.

Lessons 1c for beginners and practicing accountants

Attention

Next, on the Costs tab, check the box Performing work, providing services to customers, we must indicate the account for accounting for the main costs so that documents are filled out automatically in the future. When all the parameters are filled in, click Record and close: How to set up an Accounting policy for the provision of production services in 1C 8.2, see the following video: How to reflect the performance of production services in 1C 8.3 In order to draw up documents on the performed production services for the customer in the 1C 8.3 Accounting 3.0 there are several options. Option 1 For example, through the Production section. This section is used to account for production services that have a planned cost.

This is analytical accounting, that is, the cost of each item is calculated. So, it can be services for the production of products from customer-supplied raw materials.

Accounting info

- Act on the provision of production services;

- Invoice;

- Universal transfer document (UPD), which replaces the first two.

- Implementation (acts, invoices).

- Provision of services.

- Provision of production services.

- 1 Setting up an accounting policy

- 2 How to reflect the performance of production services in 1C 8.3

- 2.1 Option 1

- 2.2 Option 2

- 2.3 Option 3

- The act of providing services;

- Act on the transfer of rights;

- Invoice;

- Universal transfer document (UPD);

- Set of documents.

Important

Nomenclature group – object for which the service is performed:

At the bottom of the window, click the Issue invoice tab, after which the document will be generated automatically in 1C 8.3. When posting the document Provision of production services, the program 1C 8.3 Accounting 3.0 writes off costs based on the planned cost. In the case when there is no sale in the current month, but there are costs incurred, they are recognized as work in progress, and therefore are not written off to the financial result.

After all the actions performed, if you click Write, then in the Print tab, the following will become available:

When all the documents are signed, the work is accepted, click Submit and close.

Formation of the cost of services in the program 1c: accounting 8.0

Info

Revenue from the provision of services is recognized as income ordinary species activities as of the date of provision of services to the customer, which, as a rule, is formalized by signing an act on the provision of services with the customer (clause 5, clause 12 PBU 9/99). In the 1C:Accounting 8 program, the method of writing off costs from account 20 “Main production” for services rendered for accounting purposes is performed in the accounting policy settings on the “Costs” tab. The following documents can be used to reflect the implementation of services:

With the help of the document "Provision of production services" it is possible to form the cost of the sold service at the time of its provision at the planned price.

At the end of the month, the planned and actual cost will be adjusted and the identified deviations will be written off to the sales accounts.

Provision of production services in 1s 8.3

These are services for which the planned cost price has not been determined, i.e. the costs for their provision are written off by the routine closing operation of the month, and at the time of sale only revenue is recorded and the Methodology for writing off the costs for the provision of services is configured accounting policy organizations: I.e. first, it is indicated whether the costs of performing work (rendering services) to customers are taken into account, and then a write-off method is selected: excluding revenue, taking into account revenue from services, or taking into account revenue only from production services (i.e., for those services for which it is determined planned cost). 1. Reflection of the sale of services using the document "Sales of goods and services". The document "Sales of goods and services" - in fact universal document to reflect the implementation of various goods and materials, including services.

Cost calculation in 1s 8.3 accounting 3.0

Courses 1C 8.3 and 8.2 "Training 1C Accounting 3.0 (8.3)" Accounting for materials and production "Provision of production services in 1C 8.3 Production services is a section that is given considerable attention in the program 1C 8.3 Accounting 3.0. Consider how to reflect the provision of production services in 1C 8.3 using an example. Content

Setting up an accounting policy It is important to start by setting up an Accounting Policy.

To do this, click the Main tab and select the Accounting policy section, which is filled out on the basis of the order “Accounting policy for tax purposes for the current period” (usually a year), which is signed by the director of the organization.

We enter the section Implementation, subsection Services (act). As in the first case, we fill in all the available details: After clicking Write, the following documents will become available for printing:

After posting the document, the following postings for production services will be generated in 1C 8.3: The financial result will be determined after the operation Closing the month: How to close the 20th account when writing off costs “Taking into account revenue only for production services” in 1C 8.3 is discussed in the article “Why are they not closed 20 and 25 accounts at the end of the month in 1C 8.3 ".

Planned prices Due to the fact that the 1C program distributes costs for the cost in proportion to the planned cost, it must also be set. You can reflect this by setting item prices. This document is located in the Warehouse section. Please note that when filling out this document in the header, you must select a price type that is separate from the others.

You can create it yourself and specify any name. For our example, the name will be Planned. Additional expenses Please note that 1C calculates not only the cost of finished products, but also the cost of materials. Suppose we bought a cubic meter of boards 20x100x6000 for 6,000 rubles.

In total, we received 83 boards, worth 72.29 rubles. But we also paid 1,000 for shipping (other than shipping, there may be other costs).

Manufacturing plants Those who have chosen for their main activity directly the manufacture of finished products or semi-finished products are faced with the task of reflecting and registering such business processes in regulated accounting. In this article, we offer step by step instructions accounting for the production and release of finished products 1C 8.3 using the configuration "1C: Enterprise Accounting, edition 3.0".

Step 1: Verify Production Functionality

To begin with, let's make sure that our configuration allows you to keep records of the release of finished products in 1C 8.3.

In the "Administration" in the settings, go to the link "Functionality".

We are interested in the functionality of the production accounting system, which can be found on the corresponding tab.

We see that in this part the functions are used and cannot be turned off. At this point, we consider the first step completed.

Step 2: set up an accounting policy

The setting is also implemented in the main menu of the system from the "Main" section, the "Settings" subsection, the "Accounting policy" hyperlink.

The accounting policy is configured for a specific organization, then we pay attention to the types of activities for account 20 and set the flag for accounting for the release of goods.

Note! At the bottom of the figure, there are three additional options that also affect how we account:

- Accounting for deviations - the inclusion of this flag means the use of account 40 “Output of products (works, services)” in accounting;

- In terms of semi-finished products - the inclusion of this flag means accounting for multi-processing production and requires setting the sequence of processing steps;

- Services to own subdivisions - enabling this flag means that counter issue is taken into account, and requires setting up the "Counter issue" register in order to prevent the calculation of the cost of goods from looping.

We are considering a variant without the use of account 40, counter issues and semi-finished products.

This step is completed, we have completed the necessary policy settings.

Step 3: register issues at the planned cost

In the main menu of the system, the "Production" section is responsible for accounting for production processes, and a separate subsection is dedicated to the release itself.

- Requirement-invoice - allows you to register the transfer of materials to production or any other write-off of them for costs. The issue can be registered without it, but it depends on the production business process;

- Production report for a shift - registers the release according to the planned s / s and at the same time write off materials for production.

Let us analyze in detail the work with the production report for the shift.

Let's create a new document and fill it in taking into account the release of one type of goods according to a simple production specification.

In the header, in addition to the name of the company and the warehouse where the material is taken from and where the released goods are placed, you will need to indicate the cost account and the production cost unit.

To fill in the tabular part, indicators must be entered into the system in the nomenclature reference book, which will contain information about the varieties of manufactured goods.

The item card must have the form "Products". For separate accounting on the cost account of the main production, you must fill in the item group. To write off materials for manufactured products automatically, you need to fill out a specification, which can be created directly from this card.

Our next action is to put in the “Products” plate, the quantity of release, put down the planned price, specification. The lines “Account account” and “Nomenclature group” will be filled in automatically according to the data of the item card.

To write off materials and add them to the composition of the s / s, the “Materials” tab is filled out. If there is a specification, filling will occur automatically by clicking the "Fill" button.

This accounting step should be completed by holding the created form. The postings generated by this reflect the accounting for production and the release of finished products in 1C 8.3.

Analyzing the postings, we see that the planned cost is reflected in the credit of account 20, and the actual costs are collected in the debit of account 20. For a correct calculation, you need to understand the actual cost of finished goods.

Step 4: calculate the actual cost of production

Before calculating the actual s / s, the system must reflect all the necessary costs on the account of the main production. In addition to raw materials, this may be the salary of workers, depreciation of equipment, and other expenses. This calculation is triggered through the "Closing of the month".

Calculation of the current is possible with the calculations of previous periods.

If the period is closed without errors, then all transactions are displayed in green. To check the calculation of the cost price, let's see what postings were formed upon closing the cost accounts. To do this, select the appropriate operation "Show Postings".

The calculation made an adjustment to the output, this is reflected in the first posting. The posting generates a reversal entry because The planned cost was more than the actual cost.

Step 5: analyze reports on the actual cost of goods

In conclusion, it remains for us to make accounting reports on expense accounts and finished goods. Earlier, in our example, we did not reflect work in progress, assuming that all products were released to the warehouse and there were no unprocessed raw materials left in the workshops of the enterprise. This means that the balance of the main production account should be zero, and the actual cost of output was formed on the account of finished goods.

We see that account 20 is closed.

The calculation was done correctly. The next step will be accounting for the sale of finished products in 1C 8.3.

- Interpretation of dreams: why dream of swimming in the sea?

- Useful properties of onions: contraindications, benefits and harms Is it useful to eat raw onions

- Download program for flv files

- Why dream that you are cheating on a guy?

- Carrot dishes that will make you crazy What to bake from carrots quickly and tasty

- How can you treat a sore throat at different times during pregnancy: tablets, lozenges, sprays and rinses

- What does the phrase “evening in the hut” mean, what should be answered?

- The principle of operation of the gas generator - gas generator

- Norms of consumption and consumption of hot and cold water per person per month without a meter, norms of water disposal snip

- Monthly norms of water consumption per person

- Proper nutrition and exercise is the key to harmony

- How to eat right to lose weight

- Catalonia's struggle for independence

- The most unusual animals in the world The most amazing creatures of the planet

- Redcurrant jelly without cooking - recipes Redcurrant jelly in a blender

- Spicy canned cucumbers with chili ketchup "Torchin"

- Recipes and preparation of lush pancakes on kefir

- Blackcurrant jam recipes for the winter, currant jam Currant jam with lemon for the winter

- Roast beef tenderloin

- Candied pumpkin simple. Sweets from pumpkin. How to cook candied fruit, sweets, marmalade, marshmallow, pumpkin chips at home? Candied pumpkin in chocolate icing: recipe with photo