Application form for refund of overpaid tax. Instructions: We draw up an application for offsetting overpayment of taxes. Thus, it turns out

ON THE. Macepuro, lawyer

Instructions for the refund of tax overpayments The procedure for offsetting and refunding overpaid tax payments The court decisions mentioned in the article can be found: "Judicial practice" section of the ConsultantPlus systemOverpayment of tax payments occurs in almost all organizations and entrepreneurs. Someone, for example, simply made a mistake in the payment. Someone filed an updated declaration with a reduced amount of tax payable. And for someone, advance payments made during the year exceeded the amount of tax at the end of the year. Overpayment in all these cases can be returned or set off against other tax payments ipodp. 5 p. 1, p. 3 Art. 21, paragraph 1 of Art. 78 of the Tax Code of the Russian Federation. How to do this will be discussed. But we will tell you about the offset and refund of tax payments excessively collected from you by the tax authority, and taxes paid as a tax agent, in the next issues.

When an overpayment occursA tax overpayment may result from your excessive payment of any tax payments: taxes, fees, advance payments, penalties, tax penalties. 1, 14 Art. 78 of the Tax Code of the Russian Federation. Let's look at a few examples of such situations:

- when paying tax, you made a mistake in the amount and transferred more to the budget than was necessary.

Keep in mind that if the type of payment, BCC, OKTMO (OKATO) or the status of the payer was incorrectly indicated in the payment, then such a payment can simply be clarified. You need to submit an appropriate application to the IFTS. And then the inspection will correct the data in the personal account card and there will be no penalties. 7 art. 45 of the Tax Code of the Russian Federation;

- advance payments paid by you during the year exceeded the amount of tax calculated at the end of the year (for example, for income tax, for tax under the simplified taxation system);

- you found an error in the last period (for example, you forgot to apply the benefit) and filed an updated tax return for this period. 1 st. 81 of the Tax Code of the Russian Federation;

- you submitted a VAT return to the IFTS with the amount of tax to be reimbursed declared in it. If at the same time you delayed filing an application for a refund or offset (that is, you filed it when the IFTS had already made a decision on tax refunds), then the VAT refund and credit are made in the manner described below, paragraph 14 of Art. 78, paras. 6, 11.1 Art. 176 of the Tax Code of the Russian Federation.

If an application for a VAT offset (refund) is filed before the inspectorate makes a decision to refund the tax, then the VAT offset (refund) is made according to special rules (in particular, within a shorter period of time) paragraphs. 7-11 Art. 176 of the Tax Code of the Russian Federation.

If you want the tax overpayment to be offset against future payments for the same tax (that is, within the same CCC and OKTMO), then you do not need to apply to the IFTS for a credit. Such a offset will be made in your personal account card automatically as soon as the next accruals or receipts for this tax are reflected in it. You simply once again transfer to the budget less than necessary, by the amount of the overpayment.

Therefore, in case of excessive payment of tax, it makes sense to apply for its offset or refund only if the amount of the overpayment is significant or you have already ceased to be a payer of this tax.

What are the rules for counting?There are only two basic rules according to which the overpayment is credited towards the payment of future tax payments or arrears.

RULE 1. An overpayment formed by an organization or an entrepreneur as a taxpayer can only be offset against a payment that is paid by them also in the status of a taxpayer ap. 1.2 Guidelines, approved. By order of the Federal Tax Service of December 25, 2008 No. MM-3-1 / 683@ (hereinafter - Methodological recommendations). Therefore, the taxpayer cannot set off the overpayment against the payment of tax, which he must transfer as a tax agent, and vice versa 1-69.

RULE2 at the expense of local hp. 1 st. 78 of the Tax Code of the Russian Federation. At the same time, it does not matter that taxes were credited to budgets of different levels (for example, income tax is partially paid to the federal budget, and partially to the budget of a constituent entity of the Russian Federation).

For clarity, we will show in the table how an overpayment of taxes (fees) and penalties on them can be credited.

| Taxes (fees) and penalties for which there is an overpayment | Taxes (fees) and penalties against which the overpayment can be set off |

Federal taxes (fees):

|

In the account 1, 14 Art. 78, paras. 6, 11.1 Art. 176 of the Tax Code of the Russian Federation:

|

| Penalties on federal taxes | |

Regional taxes:

|

In the account 1, 14 Art. 78 of the Tax Code of the Russian Federation:

|

| Interest on regional taxes | |

| Local tax - land tax, including advance payments | In the account 1, 14 Art. 78 of the Tax Code of the Russian Federation:

|

| Penalty on land tax |

As for the overpayment of tax penalties, it follows from the Tax Code of the Russian Federation that it can generally be used to pay future tax payments or to pay off any tax debts and so on. 1, 14 Art. 78 of the Tax Code of the Russian Federation. At the same time, the type of tax (fee), penalty interest, fine, in the payment of which overpayment of fines can be credited, is not specified. This means that it is possible to offset against any tax payments.

However, there are often problems with such a credit in the field.

Recall that the amount of tax fines, depending on the type of violation, are established:

- in a fixed amount. These are, in particular, fines under paragraph 1 of Art. 116, Art. 119.1, para. 1, 2 art. 120, articles 125, 126, 129.1 of the RF Tax Code;

- based on the amount of unpaid tax (fee). For example, penalties under Art. 119, paragraph 3 of Art. 120, Art. 122 of the Tax Code of the Russian Federation.

And the tax authorities often agree to set off the overpayment of the last fines only if the principle of compliance with the types of tax is observed. 1.2 Guidelines. That is, if a fine, for example, was imposed for failure to submit a “profitable” declaration, then the overpayment of such a fine is credited only towards the payment of federal taxes (penalties on them). And vice versa: the overpayment of federal taxes (penalties on them) is credited only towards the payment of fines on federal taxes.

In connection with the ambiguous solution of this issue in practice, we asked the opinion of the specialists of the Federal Tax Service on how all the same offsets for fines should be made.

FROM AUTHENTIC SOURCES

Counselor of the State Civil Service of the Russian Federation, 2nd class

“Some fines also apply to types of taxes. Thus, the penalty for non-payment of taxes, provided for by Art. 122 of the Tax Code of the Russian Federation, refers to the federal, regional or local type, depending on what type of tax it is imposed for non-payment. This is determined by the budget legislation. A general rule applies here: federal taxes are credited against federal taxes, etc. At the same time, there are fines (most of them) that are not related to a particular type of tax (for example, all the fines provided for in Chapter 18 of the Tax Code of the Russian Federation, Article 126 Tax Code of the Russian Federation, etc.). In my opinion, it is impossible to set off these fines in correspondence with the types of tax payments related to the federal, regional or local type.

In order not to face a refusal to offset the overpayment of a fine imposed on the basis of the amount of unpaid tax, immediately ask for its return or for its offset against the payment of taxes and penalties of the same type as the tax on the basis of which the fine was calculated.

How much overpayment can be credited or refundedYou can set off or return only the overpayment that is listed in the tax authority in your personal account card. That is, the difference between the amount of receipts for a specific tax (fee, penalty, fine), including as a result of an offset, and the amount of accruals for the same tax (fee, penalty, fine), reflected on the basis of your reporting, decisions based on the results of a tax audit and other documents.

At the same time, everyone knows that the data of tax authorities and payers often do not match. Therefore, before submitting an application for a tax refund or offset to the tax office, it is better to first conduct a joint reconciliation of calculations with the budget with it, or at least request a certificate on the status of such calculations in subpara. 5.1 p. 1, p. 2 art. 21, sub. 10, 11 p. 1 art. 32, paragraph 3 of Art. 78 of the Tax Code of the Russian Federation. If you do not do this and submit an application to the tax office for a larger amount than according to the tax authorities, the IFTS will still offer you to conduct a joint reconciliation. And most likely, they will return the application to you so that you submit a new enp after verification. 3.2.2 , 3.3.4 , 3.4.6 Methodological recommendations . True, you are not obliged to do this, it is enough and the application already submitted is yap. 4 tbsp. 78 of the Tax Code of the Russian Federation; Letter of the Ministry of Finance dated September 20, 2012 No. 03-02-07 / 1-226.

The reconciliation act is prepared 10-15 business days from the date the IFTS receives your application, and a certificate of the status of settlements - up to 5 business days (however, the IFTS does not threaten anything for violating these deadlines) p. 6 art. 6.1, sub. 10, 11 p. 1 art. 32 of the Tax Code of the Russian Federation; pp. 3.1.2, 3.4.3, 3.4.4 of the Regulation, approved. Order of the Federal Tax Service of September 9, 2005 No. SAE-3-01 / 444@. These documents will indicate the amount of the overpayment, if any. They can be returned or set off against other tax payments.

Unlike a certificate of the status of settlements, the reconciliation act is a two-sided document. If you confirm your correctness if there are discrepancies in the amounts, then the tax authorities will correct the data.

But if you have a tax arrears (fee, penalties, fines) of the same type for which there is an overpayment (see rule 2 above), then the overpayment is primarily directed to pay off this debt. 5, 6 art. 78 of the Tax Code of the Russian Federation. The tax authority makes such a set-off independently with a notice to the organization or entrepreneur of the decision taken within 5 working days from the date of its adoption. 6 art. 6.1, paragraph 9 of Art. 78 of the Tax Code of the Russian Federation. But payers are not prohibited from asking for such a set-off for their part. 5 st. 78 of the Tax Code of the Russian Federation.

Moreover, if you have such a arrears, then you should not wait for the IFTS to make a “forced” offset. Since she can delay this, and at this time, pen ip will be charged on the amount of arrears. 1 st. 75 of the Tax Code of the Russian Federation. After all, the obligation to pay tax is considered fulfilled from the moment this tax is paid or from the moment the tax authority decides to offset the ep. 3 art. 45 of the Tax Code of the Russian Federation.

That is, if there are both arrears in one tax and overpayments in another, interest on the arrears is still charged. In the case when the arrears and overpayments were formed for different taxes of the same type and the arrears are repaid by offset, the tax authorities stop accruing penalties from the date of the decision on the offset Letter of the Ministry of Finance dated 07.25.2011 No. 03-02-07 / 1-260. But there are courts that do not agree with this and believe that due to the presence of an overpayment, penalties should not be charged in this situation; FAS SZO dated May 16, 2011 No. A42-4246 / 2010. Therefore, such penalties can be challenged.

How long does it take to apply for a refundYou can apply to the IFTS for a refund or offset of an overpayment opp. 7, 14 st. 78 of the Tax Code of the Russian Federation:

- the overpayment was formed due to an error in the amount in the payment order or as a result of the submission of a clarification in connection with the introduction of changes in previous periods - within 3 years from the date of payment of the tax in an excess amount;

- you want to set off or return advance payments that exceeded the amount of tax for the year - within 3 years from the date of filing the declaration for the year (but no later than the last day of the period during which it should have been submitted) -4-7/2807; Ministry of Finance dated 06/15/2012 No. 03-03-06 / 1/309; Resolution of the Presidium of the Supreme Arbitration Court of June 28, 2011 No. 17750/10;

- you want to set off or return the VAT declared in the return for reimbursement - within 3 years from the date of submission of this return. 1 st. 176 of the Tax Code of the Russian Federation.

For a refund or offset of a tax overpayment, you need to contact the Federal Tax Service at the place of your registration. 2 tbsp. 78 of the Tax Code of the Russian Federation.

On what basis you should be registered with the IFTS, the Tax Code of the Russian Federation is not specified. Therefore, we can conclude that you can apply for an offset (refund) of an overpayment to any IFTS in which you are registered, regardless of the location of which IFTS the overpayment occurred. And for example, in the event of an overpayment of tax at the location of a separate subdivision, you can, at your choice, contact either the IFTS at the location of the parent organization, or the IFTS at the location of the separate subdivision Letter of the Federal Tax Service dated 11/19/2010 No. YaK-37-8 / 15939; Decree of the FAS MO dated 10/14/2011 No. A40-99747 / 10-4-476.

Whether this is so, we checked with a tax specialist.

FROM AUTHENTIC SOURCES“If the tax is overpaid at the location of a separate subdivision, then the organization has the right to choose where to apply for a refund (offset) of the amount of overpaid tax: either at the IFTS at the location of the organization, or at the IFTS at the location of the subdivision.”

If you are registered with several inspections, then for a set-off or refund of the overpayment, it is better to contact the IFTS at the place where the tax was overpaid. And if one of the inspections independently revealed the overpayment by sending you a notice, then this IFTS should be addressed to your application for offset (refund) Letter of the Ministry of Finance dated 07/12/2010 No. 03-02-07 / 1-315

For a sample application for a credit and tax refund, see:The form of an application for a refund or offset of a tax overpayment is arbitrary. It can be submitted either on paper or electronically with an enhanced qualified signature of UP. 4, 6 art. 78 of the Tax Code of the Russian Federation. Documents confirming the overpayment must be attached to the application. These are copies of payments and declarations.

How long does it take for the IRS to make a decision?She has to do it. 6 art. 6.1, paragraphs. 4, 8 art. 78 of the Tax Code of the Russian Federation:

- at the suggestion of the tax authority, reconciliation of settlements with the budget was carried out - within 10 working days from the date of signing the reconciliation act;

- reconciliation was not carried out - within 10 business days from the date of receipt of your application (for example, when you submitted it on the basis of a notice received from the Federal Tax Service of the Inspectorate of the existence of an overpayment);

- you filed an application on the basis of the declaration (simultaneously with it or before the end of its verification) - within 10 working days from the date of the end of the in-house verification of the declaration or the expiration of the 3-month period allotted for such verification; Letter of the Ministry of Finance dated July 3, 2013 No. 03-02-08 / 25502. True, the Presidium of the Supreme Arbitration Court indicated that the terms for the return (offset) are provided for in Art. 78 of the Tax Code of the Russian Federation only for those cases when, at the time of receipt of the application from the payer, the amount of the overpayment has already been established by the tax authority. 11 of the Information letter of the Presidium of the Supreme Arbitration Court of December 22, 2005 No. 98. From this we can conclude that when an application is submitted on the basis of a declaration, the 10-day period for making a decision on offset or return does not apply at all. After all, the fact of overpayment still needs to be checked.

Therefore, we clarified with the specialists of the Federal Tax Service how long after the end of the desk audit (or the 3-month period established for its conduct), the Federal Tax Service must make a decision on offset - immediately (that is, no later than the next day) or in within 10 working days.

FROM AUTHENTIC SOURCES“In a situation where an application for a refund (offset) of overpaid tax is filed on the basis of a tax return, the deadline for the tax authority to make a decision on the refund (offset) of tax is 10 working days from the date of completion of the desk audit of this declaration or from the date of completion of the 3rd - a month of time allotted for carrying out such an inspection, - depending on what time period comes earlier e” .

Counselor of the State Civil Service of the Russian Federation, 2nd class

The IFTS must inform you of the decision made within 5 working days from the date of its adoption. 6 art. 6.1, paragraph 9 of Art. 78 of the Tax Code of the Russian Federation; Appendix No. 7 to the Order of the Federal Tax Service of December 25, 2008 No. MM-3-1 / 683@.

If you want to set off the tax overpayment against the upcoming payments of another tax of the same type, then the offset application must be submitted at least 10 working days before the deadline for paying this other tax, and preferably even more in advance. After all, if the IFTS decides to offset later than the tax payment deadline, then from the day following the day of payment of this other tax, until the date of the offset decision, penalties and

The overpaid amount of tax can be returned to the current account. For a sample application for a refund of overpaid tax in 2018 and the deadline for its submission, see the article.

Overpayment in the budget can occur for various reasons. Firstly, the company or individual entrepreneur mistakenly transferred more taxes than they should. Secondly, the tax authorities have collected too much. Most often, this is a situation when an additional amount was charged on verification. And then the company or individual entrepreneur managed to cancel additional charges through the Federal Tax Service or in court.

Tax authorities are not required to return tax overpayments older than three years to companies. The inspectors will refuse to refund, even if they insist on the fact that they forgot to inform the organization about the presence of an overpayment. So decided the Supreme Court (determination dated August 30, 2018 No. 307-KG18-12491). Details.

Regardless of what was the reason, the company or individual entrepreneur has the right to return the overpayment to the current account (Article 78 of the Tax Code of the Russian Federation). To do this, you need to contact the IFTS at the place of registration with an application. You can download the form and sample application for the refund of the amount of overpaid tax for 2018 in the article.

Application form to the tax office for a refund of overpaid tax for 2018The Federal Tax Service of Russia approved a new form for offsetting and refunding overpayments by Order No. ММВ-7-8/182@ dated February 14, 2017. The tax authorities added the wording "insurance contributions" to the title of this document. Since since 2017, contributions have come under the control of the Federal Tax Service, and the procedure for their return is now the same as for taxes.

The full name of the new document is - an application for the return of the amount of overpaid (collected, reimbursable) tax (fee, insurance premiums, penalties, fines). The application can be submitted to the inspection on paper or in electronic form (via telecommunication channels). The recommended application was approved by order of the Federal Tax Service of May 23, 2017 No. ММВ-7-8/478.

In form, the statement became similar to declarations: each number and letter in a separate cell. In addition, there are additional details:

- Document Number. Number the documents in order;

- tax (settlement) period. Specify the code of the period in which the overpayment occurred. The rules are the same as for payments. If there is a specific due date for the tax, write it down;

- inspection code. Enter the inspection that you are asking for a refund.

The updated application consists of three pages. On the first one, they give the TIN, KPP and the name of the company that applies to the tax office. Immediately bring the BCC of the overpaid tax and the period of its occurrence, the amount to be returned and the number of sheets of application documents. Entrepreneurs enter their full name and TIN.

Answered by Andrey Kizimov,

Acting State Councilor of the Russian Federation, 3rd class, Candidate of Economic Sciences

“The tax for the taxpayer can be transferred to the budget by any other person: an organization, an entrepreneur or a person who is not engaged in business. In the same way, you can pay contributions for mandatory pension, social and medical insurance. However, the right to set off or return funds transferred to the budget for taxpayers and payers of insurance premiums, third parties ... .. "

On the second sheet indicate the full name of the recipient organization or full name of the merchant, account details - the name of the bank, name and account number, correspondent account, BIC. See the following section for a sample application for a refund of overpaid tax in 2018.

If an individual returns money from the budget, then you still need to fill out the third sheet. Companies and entrepreneurs do not fill out the third sheet.

Application for the refund of the amount of overpaid personal income tax: sample 2018If the company has paid personal income tax ahead of schedule and it has no other federal tax debts, it is safer to return the amount from the budget. Although the inspectors do not recognize the amount as tax, they do recommend that you submit an approved refund claim form.

The editors warn: the Ministry of Finance allowed companies to set off the overpayment of personal income tax against future payments, but put forward a special condition

“The overpayment of personal income tax can be offset against future payments on this tax. But only if we are talking about the amounts that the organization unnecessarily withheld from employees and transferred to the budget. If the tax was overpaid due to an error in the payment, it cannot be set off against future payments.

Sample application for a refund of the amount of overpaid tax in 2018

The time for applying for a refund is limited. Three years have been allotted for this from the date of payment of the excess amount or from the day when she became aware of the excessive recovery. If this deadline is missed, the inspectors will not return the overpayment (decree of the Arbitration Court of the East Siberian District dated November 1, 2016 No. Ф02-5816 / 2016).

An application can be submitted to the inspectorate in three ways:

- personally;

- by mail with a valuable letter with an inventory;

- in electronic form via telecommunication channels or through the personal account of the taxpayer.

The inspectorate must make a decision on the return of the overpayment within 10 working days. Either from the day when the application was received from the company, or from the day when the reconciliation act was signed.

Read more in the lecture in the program "" in the course "Rules for paying taxes"

When the tax authorities will not accept a refund applicationThe list of grounds for refusing to refund an overpayment is given in Articles 78 and 79 of the Tax Code of the Russian Federation. So, inspectors have the right to refuse a refund if the company:

- submit an application to the wrong inspection, where it is registered;

- ask to set off taxes of different levels among themselves (for example, federal tax against regional tax, or vice versa);

- asks to return the overpayment, but she has tax arrears, as well as arrears in penalties and fines;

- missed the deadline for submitting an application.

But if the company submitted an application in any form, the tax authorities have no right to refuse to accept it. Indeed, in the Tax Code there is no requirement to submit an application strictly in the prescribed form (Articles 78 and 79 of the Tax Code of the Russian Federation). But inspectors still recommend using a form that is approved by the Federal Tax Service.

Usually, an application for a refund of the amount of overpaid tax occurs after the completion of the periods for submitting tax reports and transfers, when, as a result of rechecking the amounts sent to the tax office, it turns out that for some reason an overpayment has occurred.

FILES

A variety of circumstances can lead to tax overpayments. Most often, these are banal errors in the preparation of documents that are made by both company accountants and tax inspectors themselves. For example, the current tax rates are indicated incorrectly, exemptions are not applied, all the necessary values are not taken into account when calculating the taxable base, etc.

It happens that the tax authorities write off the tax twice - this usually happens if one legal entity has several accounts. There may also be situations when excessive payment of tax occurs as a result of advance payments paid on time.

In any case, regardless of the reason that led to the overpayment of tax, the law provides for the possibility of returning the amount paid in excess of the required amount. To do this, you just need to submit an appropriate application to the territorial tax office.

Deadlines for the refund of overpaid taxThere is a clearly limited period for applying for a refund of overpaid tax: three years.

If the fact of the overpayment was revealed later or the taxpayer for some reason could not apply for a refund for this period, it will hardly be possible to do anything in the future.

If the application is submitted on time and in accordance with all the rules, while the tax authority did not have any questions and it agreed with the taxpayer's request, the refund must be made no later than one month after the application was submitted.

If you don't apply for a refundIf there is no requirement to return the overpaid tax, tax inspectorate specialists have every right to offset this amount against the taxpayer's future tax payments or cover any of his arrears, penalties and fines with it.

There are situations when the application is received after the tax authorities have already disposed of the overpaid money - in such cases, only the difference between the covered arrears (penalties, fines) and the overpaid amount will be returned to the tax payer's account.

Return procedureFor example, if there was an oversight on the part of the accountant of the enterprise, which was subsequently discovered, it is necessary to prepare and submit an updated declaration to the tax authorities. Or you can simply draw up an act of reconciliation with the tax - if it reveals an overpayment, then you will no longer need to submit a “clarification”.

Sometimes the fact of a tax overpayment is revealed as a result - in this case, the tax office sends a written notification to the organization.

Sometimes, in search of the truth, taxpayers are forced to go to court, but as a rule, this is a last resort. However, if the fact of overpayment of tax is proved by the court, this will also serve as a basis for a refund.

Tax authorities are required to consider the application within 10 days from the date of receipt.

How to submit an applicationThe taxpayer has the right to submit the application to the tax authorities in any way convenient for him:

- personally,

- through a representative (if there is an appropriate power of attorney),

- by electronic means of communication,

- via Russian Post by registered mail with acknowledgment of receipt.

The application should be drawn up according to a special model developed and approved by the Federal Tax Service. When filling out the form, you must adhere to certain rules.

It is best to write in block letters in the document so that all the information is as legible as possible, while trying to avoid inaccuracies and errors, and if they do happen, it is better not to correct them, but to write a new statement.

A document is drawn up in two copies, one of which, after being approved by the inspector, remains in the hands of the taxpayer, the second is transferred to the tax office.

Sample application for refund of overpaid taxFirst, in the upper right part of the document, information about the addressee of the application and its author is indicated. This indicates the name and number of a particular tax office, as well as information about the taxpayer:

- surname-name-patronymic,

- residential address (according to passport)

- and a contact phone number (in case the tax officer needs some clarification).

The main part of the document concerns overpaid tax.

- name of the bank servicing the account,

- his corr. check,

- taxpayer account number.

This material contains the current form of the application form for the return of overpaid tax and a sample of its completion.

Also in this publication, the reader will find answers to important questions. When do I need to apply for a refund of the amount of overpaid tax in 2019? What form of document is relevant at the moment? From what date do I need to apply the new return application form? How long does it take to get a tax refund?

Features of the refund of overpayment of taxesWe note right away that it is realistic to return the amount of tax overpaid to the budget, but there are some nuances in the refund procedure that you should familiarize yourself with in advance. In particular, the features of the procedure for the return of overpaid tax depend on the reason for the overpayment by the individual entrepreneur or organization and the method of return. There are three options:

1. An individual entrepreneur or organization has paid an excessive amount of tax to the budget and wants to offset it against future taxes or arrears.

2. An individual entrepreneur or organization has paid an excessive amount of tax and wants to return it to their personal or current account.

3. The Federal Tax Service has collected an extra amount of taxes from an individual entrepreneur or organization and they want to either return it or offset it.

The article will consider the case of returning an overpayment of taxes to an individual entrepreneur or organization to a current account in 2019.

How can I find out about tax overpayments?Both individual entrepreneurs and organizations and the Federal Tax Service can find out whether there is an overpayment in taxes. If the Federal Tax Service is the first to know about the overpayment of taxes, then within ten working days, tax employees on the basis of clause 3 of Art. 78 of the Tax Code of the Russian Federation are obliged to notify the taxpayer of the overpayment in writing (approved by order of the Federal Tax Service of Russia dated February 14, 2017 No. MMV-7-8 / 182).

When an organization or an entrepreneur independently declares the occurrence of excess amounts paid, then in this case the Federal Tax Service Inspectorate may require the documents necessary to confirm the overpayment.

In addition, you can find out about the overpayment of taxes from the reconciliation with the IFTS. Thus, if an organization has learned about the existence of an overpayment on any tax (this may be the simplified tax system, UTII, personal income tax or VAT), then it needs to apply for a refund of the amount of overpaid tax in the form approved by the Federal Tax Service.

The legislation of the Russian Federation defines the terms during which it is possible to refund the overpaid tax or contribution:

- if an individual entrepreneur or LLC overpaid to the budget, then it is possible to apply for a refund of the overpaid amount of tax or contribution within three years from the date the payment was made;

- if the funds were erroneously debited by the IFTS, then the application deadline is shorter - within one month from the date the taxpayer became aware of this.

If the monthly deadline is missed, then the issue can be resolved only by filing a claim with the arbitration court. The time limit for filing a claim is three years. The beginning of the term is calculated from the day when the taxpayer became aware of the forced collection of the tax. In fact, this is the date the funds were debited from the organization's account.

Application for a refund of the amount of overpaid tax in 2019In order to return the overpayment of tax to the organization's current account, on the basis of clause 6 of Art. 78 of the Tax Code of the Russian Federation, an application must be submitted to the Federal Tax Service. The form of the document was approved by order of the Federal Tax Service of Russia dated February 14, 2017 No. MMV-7-8 / 182.

Please note that the application form is applicable from March 31, 2017. The new form of the form can be found on the official website of the Federal Tax Service "Nalog.ru"

The application for a tax refund consists of three sheets. It is filled in by writing each number and letter in a separate cell.

On sheet 1 indicate:

- the name of the organization or individual entrepreneur;

- CBC of tax with overpayment, including the period of its occurrence;

- the amount and number of sheets of application documents.

On sheet 2 indicate the details of the account: name, number and bank. If the return is carried out by an individual, then you will need to fill out the third sheet of the application.

It should be borne in mind that it will be possible to return the overpayment not only for taxes, but also for contributions (pension, medical and temporary disability and in connection with motherhood). The changes are due to the fact that, starting from 2017, the administration of contributions is carried out by employees of the tax service.

Note. According to paragraph 6 of article 78 of the Tax Code of the Russian Federation, the refund to the taxpayer of the amount of overpaid tax, in the event that he has arrears in other taxes, penalties, and fines, is made only after offsetting the amount of overpaid tax to pay off the arrears.

You can download a sample application for a tax refund in 2019 by clicking on this button:

You can download the 2019 tax refund application form here:

Place and methods of filing an application and the deadline for tax refunds in 2019Based on paragraphs 6 and 7 of Art. 78 of the Tax Code of the Russian Federation, you can apply for a refund within three years from the date of payment of the excess amount of tax.

The application must be submitted to the Federal Tax Service in one of the following ways:

- on paper;

- in electronic form (with an enhanced qualified signature via telecommunication channels according to the approved format).

In conclusion, we add that the tax service, on the basis of paragraph 6 of Art. 78 of the Tax Code of the Russian Federation is obliged to return the overpayment of tax within one month from the day it received an application from an individual entrepreneur or organization. Initially, within 10 days from the date of receipt of the taxpayer's application for a refund, the IFTS is obliged to make a decision on the refund of the amount of overpaid tax or on refusal to refund. Then, within 5 days from the date of the decision to return the funds or to refuse, the IFTS is obliged to inform the taxpayer of its decision.

In 2019, the documents that legal entities and individuals must use to offset and refund tax overpayments have changed. Let's take a look at what the application form for tax overpayment offset looks like now and how to fill out this document correctly.

The application forms used to offset and refund the amounts of overpaid (collected) taxes, fees, insurance premiums, penalties, fines were approved by order of the Federal Tax Service dated February 14, 2017 No. ММВ-7-8/. They should be used by both individuals and legal entities. But since 2019, minor changes have been made to the order of the Federal Tax Service, which must be remembered.

When new forms are neededAccording to article 78 of the Tax Code of the Russian Federation, taxpayers who have overpaid may dispose of the overpaid amounts in different ways:

- offset them as future payments;

- pay off the arrears on other obligatory payments;

- reduce or completely close the debt on penalties and fines for offenses;

- request a refund.

These rules apply to all fees and taxes introduced in the Russian Federation, including state duty (with some features listed in Article 333.40 of the Tax Code of the Russian Federation), VAT, advance payments. However, it must be understood that the tax service will not return or offset the overpaid amount against future payments until the debts are repaid.

Sample application letter for overpaid taxIf the taxpayer decides to redistribute his money, he needs to write an application for a tax offset. The form of this document is presented in the order of the Federal Tax Service dated Appendix No. 9. You can download it at the bottom of the page.

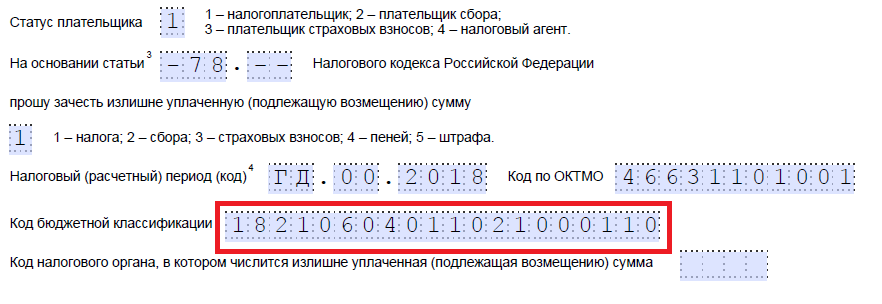

How to fill out such a documentLet's say Kolosok LLC filed a transport tax return for 2018, but made a mistake when paying it, paying 3,112 rubles more. The organization applies to the inter-district IFTS, asks for a credit for overpayment of taxes; the application writes that she would be credited with the overpaid amount on account of the upcoming payments on property tax of organizations. Consider step by step filling out such a document.

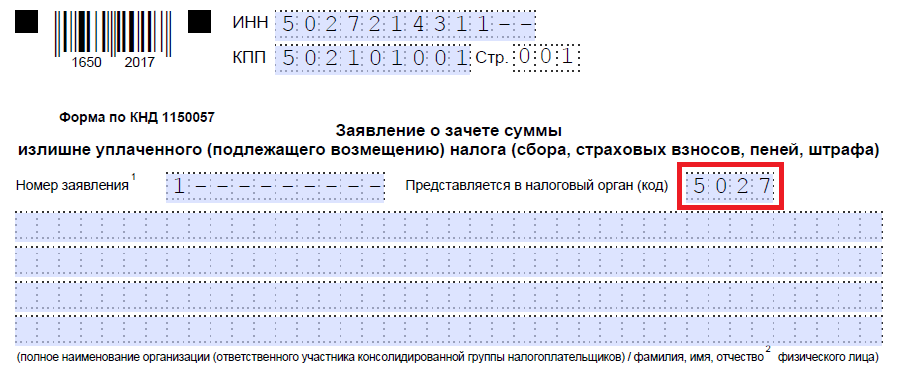

Step 1. Traditionally, at the very top, you should indicate the TIN and KPP. The IP identification number consists of 12 digits, so there should not be any free cells left. Organizations enter only 10 digits in the corresponding fields, dashes are placed in the remaining two. When filling out the line intended for the checkpoint, applicants must act in the same way: there are numbers - enter them, no - put dashes.

Step 2. We prescribe the number of the appeal. Here they put down the number of times in the current year they applied for offset. Do not forget about dashes if the number of digits entered is less than cells.

Step 3. Enter the code of the tax authority where the appeal will be sent. This should be an inspection of the Federal Tax Service at the place of registration of an individual entrepreneur or organization. In a consolidated group of taxpayers, the responsible member of this group must apply for the offset of the overpayment of income tax.

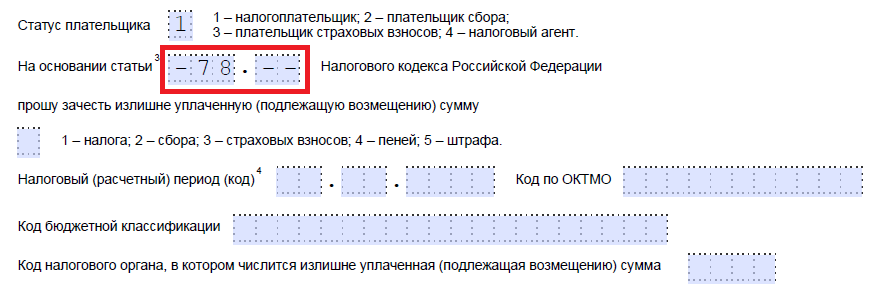

Step 4. We prescribe the full name of the applicant organization, for example, Kolosok Limited Liability Company. The remaining cells are filled with dashes. None of them should be empty. When filling in this field by an individual entrepreneur, he must indicate the last name, first name and patronymic, if any. In addition, you should indicate the status of the applicant, as whom he applies, in accordance with the instructions:

- taxpayer - code "1";

- fee payer - code "2";

- payer of insurance premiums - code "3";

- tax agent - code "4".

Step 5. We indicate the article of the Tax Code of the Russian Federation, on the basis of which offset can be made. It will depend on which payment was overpaid. The Federal Tax Service left 5 cells to indicate a specific article. If some of them are not needed, it is necessary to put dashes. Here are the options for filling out this field:

- - to set off or return overpaid fees, insurance premiums, penalties, fines;

- - to return overcharged amounts;

- — for VAT refund;

- - to return the overpayment of excise duty;

- - for the return or offset of the state fee.

Step 6. We write down exactly why the overpayment was formed - tax, fee, insurance premiums, penalties, fines.

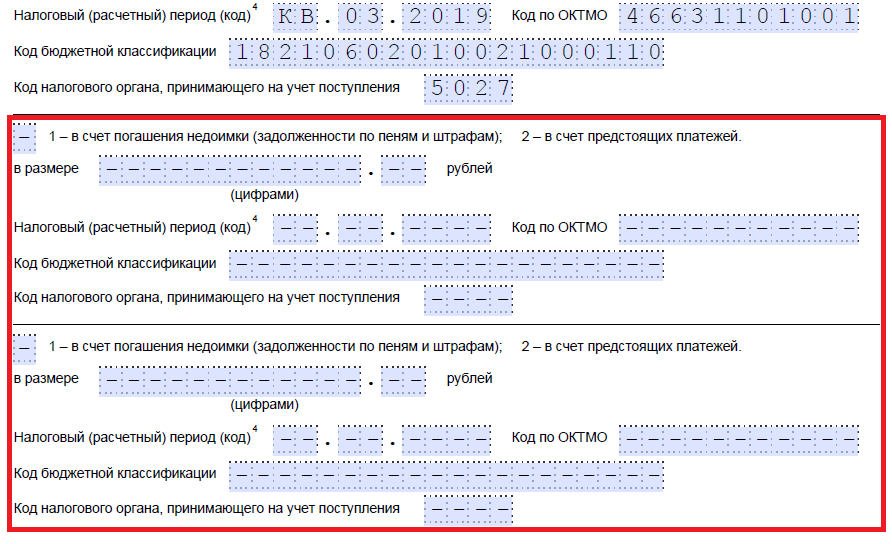

Step 7. The applicant specifies for what period the overpayment was formed. The developers provided 10 familiarity to indicate the code, of which there are two dots. The first two of them can be filled in with one of the following options:

- MS - monthly;

- KV - quarterly;

- PL - semi-annual;

- GD - annual.

Specific values will depend on the reporting period provided for by law for the payment for which the offset is planned.

In the 4th and 5th familiarity, the reporting period is specified:

- if a monthly billing period is approved for the payment, then in the provided columns enter the numerical value of the month (from 01 to 12);

- if quarterly, indicate the value of the quarter (from 01 to 04);

- for payments with a semi-annual reporting period, the values 01 or 02 are entered, depending on the semi-annual;

- for the annual fee, zero values \u200b\u200bare provided, that is, “0” must be put down in both cells.

The last four characters are for a specific year, such as 2019.

Instead of alphanumeric combinations, a specific date can also be written, for example, 01/25/2019. Such an entry is allowed if the legislation provides for a specific date for the payment of a fee or for the submission of a declaration.

Examples of filling in the billing period: “MS.02.2019”, “Q.03.2019”, “PL.01.2019”, “DG.00.2019”, “05.04.2019”.

Step 8. Enter the OKTMO code. If you do not know it or have forgotten it, you can call the Federal Tax Service at the place of registration or on the nalog.ru website to find out the required code by the name of the municipality.

Step 9. Accurately enter the BCC for the payment of the corresponding payment, using the Order of the Ministry of Finance of Russia dated 06/08/2018 N 132n. You can also find out the code using the website of the Federal Tax Service or look at it on a previously completed payment order.

Step 10. We specify to which IFTS the excess funds were transferred.

Step 11. On the first sheet, it remains to fill in how many sheets the application is submitted on and how many sheets of supporting documents are attached, as well as indicate data about the applicant himself. We recommend leaving these two small sections for later.

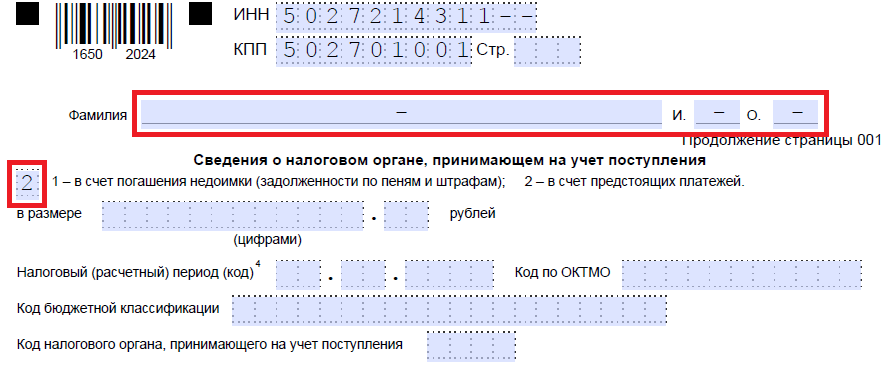

Let's continue filling on the second sheet. In the very first field, where you want to specify the last name, first name and patronymic, we put dashes. Below we indicate what needs to be done with the overpayment - pay off the debt or leave funds on account of upcoming payments.

Step 12. We write down the specific amount that the applicant wants to set off. It is indicated in numbers, without text decoding.

Step 13. Fill in the period for the payment for which it is planned to offset. In our case, the corporate property tax is quarterly, so we enter the quarter in which the overpayment should go.

Step 14. We write down the OKTMO code again. As a rule, it is duplicated.

Step 15. We specify the CCC for the transfer of funds, to which the excess amount will go. In our country, it differs from the previous KBK, since taxes are different. If the overpayment goes towards future payments for the same fee, then the BCCs are the same. An exception in the event that the codes were previously changed by decision of the Ministry of Finance. We also recall that the offset can be carried out according to certain rules: they must belong to the same type: federal, regional or local. It is impossible, for example, to set off the federal part of income tax against future sales tax payments.

Step 16. The code of the IFTS, which accepts receipts, is usually duplicated.

Step 17. Since there are no more overpayments, in our example, the following lines are not filled. You can put spaces there. Also, organizations and individual entrepreneurs do not fill out the third sheet. It is intended for individuals who are not registered as individual entrepreneurs and who have not indicated their TIN.

Step 18. We return to the first sheet and enter the number of pages and applications. In the fields provided, applicants indicate the relevant data.

Step 19. The last part of the application should not cause problems when filling out. Here it is necessary to clarify who and when submits the appeal, as well as indicate the contact phone number. The right part remains blank: it is intended for the marks of the inspectors of the Federal Tax Service.

If the entrepreneur (company) decides to return the overpayment amount, he needs to use another form from the order of the Federal Tax Service dated February 14, 2017 No. ММВ-7-8 /, proposed in Appendix No. 8. It contains a form for returning the excess amount.

The rules for filling out this document are about the same. Therefore, we will not consider them in detail, but we will give an example of a completed document. Let's say Kolosok LLC overpaid VAT for the first quarter of 2019 in the amount of 15,732 rubles and now wants to return it. This is what the appeal of the head of the LLC will look like.

When and how to applyAccording to article 78 of the Tax Code of the Russian Federation, you can apply for a set-off and a refund within 3 years from the date of payment of the fee. Documents can be delivered in three ways:

- personally;

- by mail with a valuable letter with an inventory;

- in electronic form via telecommunication channels or through a personal account.

Having received such an application, the tax authority decides whether to satisfy it or not. The service notifies the entrepreneur of its decision within 10 days from the date of receipt of the application. As a rule, if the initiative comes from an organization or individual entrepreneur, the FTS makes a reconciliation of calculations. If the inspector himself discovers the overpayment, then the reconciliation may be refused. The entrepreneur is not released from the obligation to submit an application.

: healing properties and methods of application In case of inflammation of the prostate gland, it is necessary")

- Causes of dilated pupils in a child

- Lymph nodes under the arm: causes of inflammation, which doctor to contact, treatment

- Right little finger cut

- Dill seeds for the pancreas: method of application, reviews

- Rupture of blood vessels in the hands: causes, treatment, prevention

- Why it itches - signs

- How to increase melanin in the body What foods are rich in melanin

- What foods contain melanin?

- Which foods are high in melanin Melanin is found in foods

- Is it possible to eat dates with pancreatitis: expert opinions

- Mole on the neck: features and complications, treatment

- Hellebore water from lice: instructions for use

- How to deal with swelling after an insect bite

- Are there lice on nerves?

- Wormwood in horticulture Wormwood from pests

- The use of celandine in folk medicine for the treatment of skin diseases, in gynecology. What is the fruit of a large celandine

- Deaf nettle: medicinal properties of a flower and contraindications Which plant is similar to nettle

- What is the fruit of meadow clover

- Licorice root (licorice): healing properties and methods of application In case of inflammation of the prostate gland, it is necessary

- Why does the child have dilated pupils?