1 s zup loan agreement not for an employee. Deductions from employee salaries in 1C. How to keep child support

How does a loan agreement differ from a loan or credit agreement, and how to correctly formalize the issuance of money to an employee in the program “1C: Salaries and Personnel Management 8” ed. 2.5, we wrote earlier. In this material, read the detailed recommendations of 1C experts on accounting for loans in the 1C: Salaries and Personnel Management 8 program (rev. 3.0).

Drawing up a loan agreement

The procedure for issuing and repaying a loan is determined in the loan agreement between the employee and the organization (Article 807 of the Civil Code of the Russian Federation). In accordance with Article 807 of the Civil Code of the Russian Federation, when concluding a loan agreement, the organization transfers the ownership of money to the employee, and he undertakes to return the loan amount to the organization. The loan agreement is considered concluded from the moment the money is transferred.

In the program "1C: Salary and HR Management 8" ed. 3.0 to apply for a loan there is a form with the same name - Employee loan agreement. This document sets up the calculation of material benefits, accounting for the issuance and repayment of the loan.

You can create it in the menu Salary -> Loans to employees by selecting item D from the drop-down menu employee loan clause. The loan accounting system is available in the program if Initial program setup the AND flag is set use employee loans.

Document Employee Loan Agreement consists of two parts - Issuing a loan And Loan repayment(Fig. 1).

Issuing a loan

Method of issuing a loan. The loan can be issued in one of two ways One time or In several tranches. To reflect the method of issuing a loan, you need to set the switch to the appropriate position. For a one-time loan, you must indicate the loan amount. If at the time of generating this document the loan to the employee has already been fully issued, then you can register the fact and date of issue directly in this document by checking the flag The loan under the agreement was issued in full and filling in the field date of issue. In the case when the loan is issued after the document has been processed, you can Issue a loan directly from the document form Employee Loan Agreement by following the hyperlink of the same name. This will automatically create a document Issuing a loan to an employee, in which the field will be filled Loan agreement. Besides, Create document Issuing a loan to an employee you can by selecting the menu item of the same name. Then in the document Issuing a loan to an employee You must provide a link to the document - contract. When choosing a delivery method In several tranches in the form of the document, it becomes possible to indicate in a table the months of issue and the size of the trenches. Each tranche must have a corresponding document Issuing a loan to an employee, indicating the date the loan was issued, since the day the loan was issued affects the calculation of material benefits.

After completing the document Issuing a loan to an employee, document Employee Loan Agreement becomes unavailable for editing. All changes that need to be made should be considered Changes in the terms of the loan agreement. In the document of the same name, you should indicate a link to the agreement, the terms of which are changing, and the date the changes come into force (Fig. 2).

Loan disbursement period. The loan disbursement period can be specified in two ways. The first is to set the number of months in the field For a period of, starting from the month specified in the field WITH. At the same time, a month in the field By is installed automatically. The second way is to specify the period From - To, then the number of months in the field For a period of will be calculated automatically.

In field Bid you need to set the annual interest rate on the loan.

Calculation form. The form of payment can be Cash And Cashless. When migrating data from previous versions Payment form default is considered Cash.

This field must be filled in to perform synchronization with the program “1C: Accounting 8” ed. 3.0.

Loan repayment. After setting the flag The loan was previously partially repaid The following fields become available to fill in: maturity date,Sum And Interest. According to the agreement, the employee can repay the loan either monthly or in a lump sum. The switch should set one of two options During the term (monthly payments) or .

Monthly repayment. With monthly repayments, various types of payments are possible: Differentiated, Annuity, Interest only (loan at the end of the term), Loan only, (interest at the end of the term).

Types of payments for monthly loan repayments. Differentiated payments represent a variable amount. Interest is accrued monthly on the loan balance, and the principal debt is repaid in fixed installments, calculated as the quotient of dividing the loan amount by the number of months of lending.

Annuity payments are payments fixed from month to month, the amount of which consists of part of the principal debt and interest accrued on the balance of the loan.

The meaning of the other two types of payments is clear from the name.

If only interest is paid monthly and the principal is repaid at the end of the term, then interest is calculated in proportion to the days in the month.

If the principal is paid monthly and interest is paid at the end of the term, then, as with an annuity payment, the principal is repaid monthly with a fixed amount obtained by dividing the entire principal amount by the number of months.

Principal repayment amount is calculated depending on the selected type of payment and the exact amount is indicated only for an annuity payment (in other cases, at the time of drawing up the contract, the amount of the monthly payment is determined approximately).

To see the payment amounts you need to use the report Loan repayment schedule, which can be obtained by clicking on the button Seal.

Example 1

The loan was issued in a lump sum of 200,000 rubles for a period of 10 months in May 2015 with an annual interest rate of 5%. Loan repayment is provided throughout the entire term in monthly payments.

Let's create loan repayment schedules for different types of payments, all other things being equal:

Deferred payment for monthly repayments. When repaying the loan with monthly payments, the program provides the possibility of deferred payments. If you set the flag A deferment is provided until and specify the month, then deductions will begin from the specified month. It is clear that delaying the start of payment will lead to an increase in the monthly payment. Moreover, if you install Payment limit, the term for which the loan was provided will be automatically recalculated and extended.

Repay the loan in a lump sum at the end of the term. If loan repayment is stipulated in the agreement At the end of the term (lump sum and interest), then the types of monthly payments, deferment and payment restrictions after deferment are not set, therefore they are not available for editing

Material benefit and personal income tax. A material benefit arises when the interest on a loan in rubles is less than 2/3 of the Central Bank refinancing rate (clause 1, clause 2, article 212 of the Tax Code). In the program “1C: Salaries and Personnel Management 8” edition 3.0, the Central Bank refinancing rate is stored in the information register of the same name.

From September 14, 2012, the rate is 8.25%, that is, 2/3 of the rate is 5.5%.

Thus, if the annual interest rate on the loan is less than 5.5%, the employee will receive a financial benefit. When an employee receives an interest-free loan, a material benefit also arises (letter of the Federal Tax Service dated December 20, 2011 No. ED-3-3/4211@).

The material benefit is generated on the day when the employee pays interest under the contract (clause 3, clause 1, article 223 of the Tax Code).

Usually they are withheld from his salary. If the employee does not pay interest under the agreement, the material benefit is calculated at the time of repayment of the principal debt. Material benefits are subject to personal income tax at a rate of 35%.

Material benefits are calculated automatically. But it is not always subject to personal income tax. If an employee has the right to a property deduction (a tax certificate), the material benefit is exempt from taxation on an equal basis with other income. In this case, you need to remove the flag Material benefits are subject to personal income tax, set by default.

Document Repaying a loan to an employee. Regular planned loan repayment according to the schedule is reflected in the document Payroll on the bookmark Loans. Material benefits and personal income tax are also calculated here (Fig. 7).

Document Repaying a loan to an employee is intended to register an unscheduled return of part of the loan by an employee. When filling out this document, pay attention to the field hint Sum. It reflects the outstanding principal and interest as of the date the document was created.

Despite the fact that debt repayment is made in one amount, it is taken into account and reflected in Loan repayment report it is divided separately for principal and interest (Fig. 9).

Example 2

From Loan repayment report(Fig. 9) it can be seen that 53,575.34 rubles. went to repay the main loan and 1,424.66 rubles. to pay off interest.

For more details, watch the video, which was made in “1C: Salaries and Personnel Management 8” (release 3.0.22.188) -

Question: v7: Atol 30Ф CheckType for issuing and returning a loan to an employee.

Actually the subject. What CheckType codes must be assigned to correctly reflect the issuance of a loan to an employee and the repayment of the loan by the employee?

Device: Atol 30F

FFD 1.05 Drivers version 10

It is not yet possible to download driver documentation from the Atol website, because it hangs tightly..

Answer:“providing and repaying loans to pay for goods, works, services (including pawnshops lending to citizens secured by things belonging to citizens and activities for storing things)” Hmm, it’s an interesting question what/how a pawnshop should break through when issuing an amount (loan) secured by valuables of things.

Most likely, a check for “Expenditure of money” with the type of payment in cash or electronically, in the title “Providing a loan with full name secured by collateral...”.

If the loan is repaid in cash, a “Return of Expense” check will be issued.

In case of non-repayment and sale of the collateral property to an individual or a lawyer for cash, then a regular “Parish” check as for sale.

This is probably the answer to question ().

Question: v7: ZiK 7.7 - financial benefit on the loan, without deduction for repayment of previous months.

Good day! Please help me understand the situation, which consists of several points. First, the employee was given a loan, and at the same time it is not deducted from wages, since no more than 50% can be withheld, and the employee, receiving wages, after receiving it transfers it back in full to repay the loan. Secondly, the loan was issued in April of this year for the purchase of an apartment, and it was believed that the employee had the right to a property deduction. But, in the end, it has now become known that he does not have such a right, since he used it earlier. Accordingly, the task now is to charge personal income tax at a rate of 35% on the material benefit of the loan, starting in April 2017.

As a result, a number of questions arise - how to calculate personal income tax in ZiK 7.7, starting from April 2017?

In this case, it is unlikely that the accrual of personal income tax itself will be reflected automatically? After all, the document “Enterprise Loan”, in addition to accruing personal income tax, forms “Deduction for loan repayment,” but it should not exist.

What to do in this case? If personal income tax at a rate of 35% is calculated manually, and how to reflect it, starting from April 2017?

Answer: Thank you very much guys, you helped out!

Question: ZUP 3.1 - loans.

Answer:

Question: A loan agreement with an employee is taxed at the wrong checkpoint

Answer:

Question: Verification of the user's age and loan

Hello!) This is the case, it is necessary to determine whether the user is an adult, and it is also impossible to issue loans in an amount exceeding 500,000 per day. Has anyone encountered anything like this?

Question: Automation of interest calculation on loans and borrowings 1s 8.3

Hi all!

There is Enterprise Accounting, edition 3.0 (3.0.41.48)

And you need to understand whether automation of interest calculation on loans and borrowings has been implemented? Who knows?? I can not find.

Answer:() Thanks everyone!

Question: Calculation of interest on loans in 1s 8.3

Hi all! No one knows whether the issue of calculating interest on loans has been resolved in 1C 8.3?

I have Enterprise Accounting, edition 3.0 (3_0_42_37)

But I can't find the document.

Answer: Clear. Well...

Question: ERP 2.4 Entering initial balances for loans to employees

We enter the initial balances for the salary subsystem. One of the organizations is small and we do everything manually. Everything seems to be fine, but the question arose, where to deposit the debt of employees on loans that the organization previously issued to the employee? I'm interested in the balance in the Mutual Settlement Register with Employees. I don’t see how to enter it using standard documents, except manually by moving the registers.

Issuing a loan to an employee is a fairly common case in an enterprise, and the loan can be interest-bearing or interest-free. The receipt of a loan is preceded by an agreement, which is drawn up in writing. The agreement specifies: the type of loan, the procedure for paying interest on the loan (if the loan is interest-bearing), payment methods, obligations of the parties and the procedure for resolving disputes.

Issuing a loan to an employee in 1C ZUP 2.5

In the 1C Salary and Personnel Management program, version 2.5, the issuance of a loan to an employee is reflected in the document “Loan Agreement with an Employee,” which is located on the “Payroll Calculation” tab.

In the new document, the employee to whom the loan is issued is selected. The loan amount, annual interest rate, and currency are also indicated. Here you need to enter information about loan repayment. The loan can be repaid monthly, or after a specified number of months. This setting also applies to loan interest.

In the section of the document “Regulated Accounting” the organization is indicated, the interest account is account 91 subaccount 01 “Other income”, since for the enterprise the accrued interest on the loan is income.

In the same section, check the box indicating the need to accrue material benefits.

A material benefit arises if the amount of interest for the use of borrowed funds, expressed in rubles, calculated on the basis of two-thirds of the current refinancing rate established by the Central Bank of the Russian Federation on the date of actual receipt of income by the taxpayer, exceeds the amount of interest calculated on the basis of the terms of the agreement (subclause 1 paragraph 2 of article 212 of the Tax Code of the Russian Federation).

Material benefits from savings on interest are subject to personal income tax at a rate of 35% (clause 2 of Article 224 of the Tax Code of the Russian Federation).

The document “Loan Agreement with an Employee” has two printed forms: “Loan Agreement” and “Loan Repayment Report”.

Loan repayment in 1C ZUP 2.5. reflected in the document “Payroll”. Also located on the “Payroll” tab.

Settlements on loans to employees are recorded on a separate tab “Loan repayment”. To automatically fill out the document, click on the “Fill” button. After this, we calculate the document. When calculating only bookmarks for loans, click on “Calculate” and “Calculate loan repayments”. To calculate the document in full, click on “Calculate (full calculation)”.

Setting up deductions in “1C: Salary and HR Management 8”, ed. 3.1, be it alimony, fines or loan payments.

How to keep child support

Deductions from wages are very diverse, but they can be divided into several types:- mandatory deductions, which include alimony, deductions based on writs of execution (fines), etc.;

- at the initiative of the employer, fines for violation of traffic rules, etc.;

- at the initiative of the employee, for example, deduction to pay off a loan.

If parents do not fulfill their obligations to support their children, then funds are recovered from the parents in court. In turn, the employer is obliged to withhold alimony from the employee’s salary every month and pay the person receiving alimony no later than three days from the date of payment of wages to the debtor.

The organization has received the executive documents, and we are forming the following actions in the system.

First, let's configure the system: go to the section “Settings” - “Payroll calculation” - “Setting up the composition of accruals and deductions” - “Deductions” - set the flag “Deductions under writs of execution.”

We register the terms of the writ of execution in the document “Writ of Execution”, which is located in the tab “Salary” - “Deductions”.

In the writ of execution we indicate the employee from whom alimony is required to be withheld, the withholding period, the recipient and his address, and the method of calculation. Calculation methods can be as follows

- Percentage, if the writ of execution specifies to withhold alimony as a percentage.

- Fixed amount.

- A share, if the calculation is similar to the calculation by percentage, however, allows you to avoid errors in the calculation due to rounding (for example, 1/3 instead of 33.33%).

The deduction itself is made in the document “ » when calculating wages. Further, the payment of income occurs without taking into account the amounts under writs of execution.

Fines for traffic violations

An organization can pay a fine for violating traffic rules (traffic rules) and withhold the amount from the employee’s salary in accordance with Art. 138, 238, 248 Labor Code of the Russian Federation.To do this, in “1C: Salaries and Personnel Management 8”, ed. 3.1, create a new hold. Let's go to “Settings” - “Holds”. We create a new element in the directory. In it we indicate: “Name” - “Traffic fines”. Select the retention purpose “Deduction for settlements on other transactions»; "Calculation and indicators» - the result is entered as a fixed amount; “Type of salary transaction” - “Compensation for damage”.

We enter the amount of the received fine using a special document “ Deduction for other transactions", which is located in “Salary” - “Deductions”. In the new document we indicate the organization, employee, retention period, and amount of retention.

At the end of the month we calculate the salary using the document “ Calculation of salaries and contributions", where on the tab " Holds» is automatically subject to deductions according to traffic regulations. To reflect transactions, we must register “ Reflection of salaries in accounting».

Note: transactions uploaded to the accounting program are generated automatically according to debit 70 and credit 73.02.

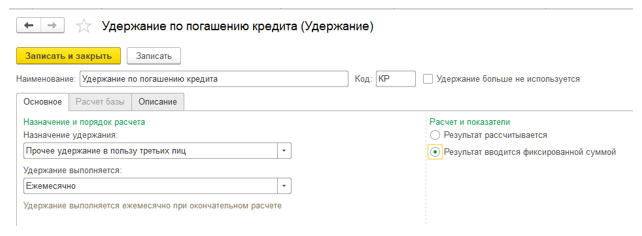

Deduction for loan repayment

At the request of an employee, an organization can reduce earnings by making transfers to other organizations, for example, paying off an employee’s loan.First of all, we set up the system: create a new element in the directory " Holds" Fill in the new element: "Name" -“Deduction for loan repayment”; "Hold Assignment" -“Other retention in favor of third parties”, “Hold in progress” - “ Monthly ", "Calculation and indicators" -“The result is entered as a fixed amount.”

In this case, it is enough to create a retention once and then apply it to all employees.

Then we register the terms of retention in the document “ Permanent retention in favor of third parties» (“Salary” - “Deductions”). Select an employee in the line “ Hold» - previously created hold. Next, set the switch to "Start New Hold", we determine the period, in the line “Counterparty” we select the recipient - the bank. We select an employee in the tabular part of the document and indicate the amount, since when creating the deduction we indicated that the result is a fixed amount.

At the time of calculating the salary for the month, the system will withhold the specified amounts from the employee. When uploading to “1C:Accounting 8”, transactions will be generated for debit 70 and credit 76.49.

Checking the withheld amounts can be done through salary reports: payslip, salary analysis, and so on.

", December 2017

Setting up deductions in “1C: Salary and 8”, ed. 3.1, be it alimony, fines or loan payments.

How to keep child support

Deductions from wages are very diverse, but they can be divided into several types:

mandatory deductions, which include alimony, deductions based on writs of execution (fines), etc.;

at the initiative of the employer, fines for violation of traffic rules, etc.;

at the initiative of the employee, for example, deduction to pay off a loan.

First, let's look at how to withhold alimony in "1C: Salaries and Personnel Management 8", ed. 3.1.

If parents do not fulfill their obligations to support their children, then funds are recovered from the parents in court. In turn, the employer is obliged to withhold alimony from the employee’s salary every month and pay the person receiving alimony no later than three days from the date of payment of wages to the debtor.

The organization has received the executive documents, and we are forming the following actions in the system.

First, let's configure the system: go to the section “Settings” – “Payroll calculation” – “Setting up the composition of accruals and deductions” – “Deductions” – set the flag “Deductions under writs of execution.”

We register the terms of the writ of execution in the document “Writ of Execution”, which is located in the tab « Salary" – « Holds."

In the writ of execution we indicate the employee from whom alimony is required to be withheld, the withholding period, the recipient and his address, and the method of calculation. Calculation methods can be as follows

Percentage, if the writ of execution specifies to withhold alimony as a percentage.

Fixed amount.

A share, if the calculation is similar to the calculation by percentage, however, allows you to avoid errors in the calculation due to rounding (for example, 1/3 instead of 33.33%).

A money transfer through a paying agent is completed if the amount withheld from the employee will be transferred to the recipient using a paying agent: bank or post office.

The deduction itself is made in the document “ » when calculating wages. Further, the payment of income occurs without taking into account the amounts under writs of execution.

Fines for traffic violations

An organization can pay a fine for violating traffic rules (traffic rules) and withhold the amount from the employee’s salary in accordance with Art. 138, 238, 248 Labor Code of the Russian Federation.

To do this, in “1C: Salaries and Personnel Management 8”, ed. 3.1, create a new hold. Let's go to “Settings” – “Holds”. We create a new element in the directory. In it we indicate: “Name” – “Traffic fines”. Select the retention purpose “Deduction for settlements on other transactions»; "Calculation and indicators» – the result is entered as a fixed amount; “Type of salary transaction” – “Compensation for damage”.

We enter the amount of the received fine using a special document “ Deduction for other transactions", which is located in “Salary” – “Deductions”. In the new document we indicate the organization, employee, retention period, and amount of retention.

At the end of the month we calculate the salary using the document “ Calculation of salaries and contributions", where on the tab " Holds» is automatically subject to deductions according to traffic regulations. To reflect transactions, we must register “ Reflection of salaries in accounting».

Note: transactions uploaded to the accounting program are generated automatically by debit and credit 73.02.

Deduction for loan repayment

At the request of an employee, an organization can reduce earnings by making transfers to other organizations, for example, paying off an employee’s loan.

First of all, we set up the system: create a new element in the directory " Holds" Fill in the new element: "Name" -“Deduction for loan repayment”; “Hold Assignment” –“Other retention in favor of third parties”, “Hold in progress” – “ Monthly ", "Calculation and indicators" –“The result is entered as a fixed amount.”

In this case, it is enough to create a retention once and then apply it to all employees.

Then we register the terms of retention in the document “ Permanent retention in favor of third parties» (“Salary” – “Deductions”). Select an employee in the line “ Hold» – previously created hold. Next, set the switch to "Start New Hold", we determine the period, in the line “Counterparty” we select the recipient - the bank. We select an employee in the tabular part of the document and indicate the amount, since when creating the deduction we indicated that the result is a fixed amount.

At the time of calculating the salary for the month, the system will withhold the specified amounts from the employee. When uploading to “1C:Accounting 8”, debit and credit entries 76.49 will be generated.

Checking the withheld amounts can be done through salary reports: payslip, salary analysis, and so on.

.png "The 1C query language is one of the main differences between versions 7.7 and 8. One of the most important points in learning 1C programming is...")

- New

- Personal income tax withheld more calculated 1s 8

- Phrasal verb get: basic meanings with translation

- Additional educational program “young traffic inspector” methodological development (grade 7) on the topic

- The verb faire in French The verb faire in all tenses

- Degrees of comparison of adjectives – Die Steigerung der Adjektive

- Regular and irregular verbs in English

- Questions in English

- Tenses and their use Use of tenses in French

- The most interesting translations of the names of cartoon characters Description of the appearance of fairy-tale characters in English

- Sentence in English (Syntax)

- Deductions from employee salaries in 1C

- 3 trade management goods movement card

- Transfer of personal income tax 1s 8.3. Generating personal income tax reporting

- The “red reversal” rule: typical mistakes and examples of application in accounting (Grigorieva E

- The registration form has been lost, what should I do?

- Accounting info How to complete product packaging in 1C

- Distribution of personal income tax payment in 1s 8

- Left and right connection 1s

- KUDiR: a terrible beast or an important document?