Accounting with the principal in 1C 8.3 goods. Agency agreement: accounting between the principal and the agent. Accounting by the agent

Almost all companies on the market now provide certain services to their clients. They can be one-time or monthly, mass or individual.

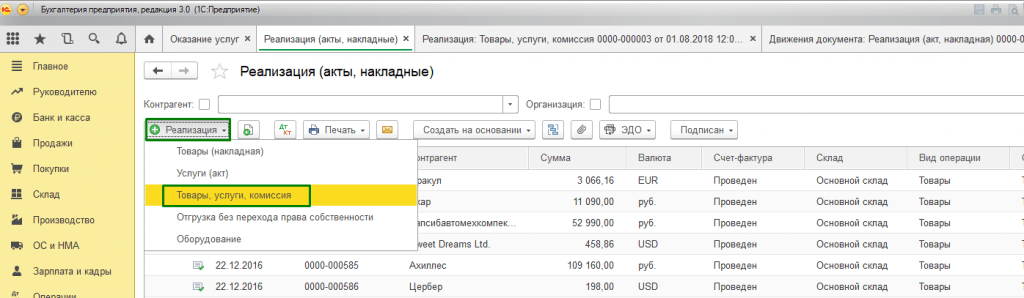

The 1C accounting program we are considering provides various ways of registering and accounting for the provision of services, for example, through “Sales (acts, invoices).” Let us give examples of the use of different methods of reflecting the provision of services.

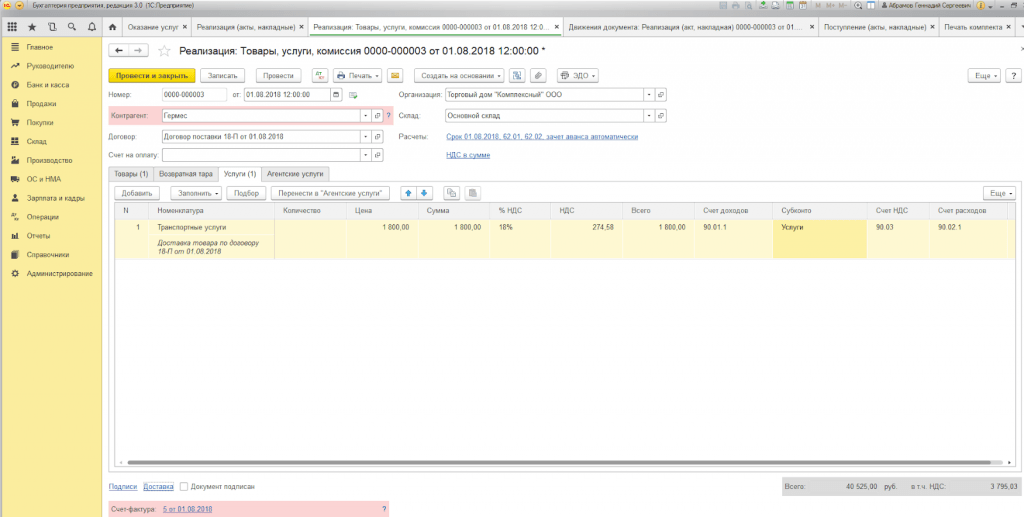

Example 1. LLC "Trading House "Complex" entered into an agreement for the supply of goods. Delivery is carried out by the company at the expense of the buyer.

For registration, we use the document “Sales (acts, invoices)”, which can be accessed through the “Main Menu – Sales”.

If it is necessary to issue a single invoice for the supply of goods with delivery, we use the “Goods, services, commission” option, which we find in the “Create” submenu.

Fill out the “Product” and “Services” tabs.

When choosing to print a set of documents, you can specify the number of copies of those forms that are used in your company's document flow.

The printed form of the act of provision of services in the 1C program is standardized, but can be developed by the company independently.

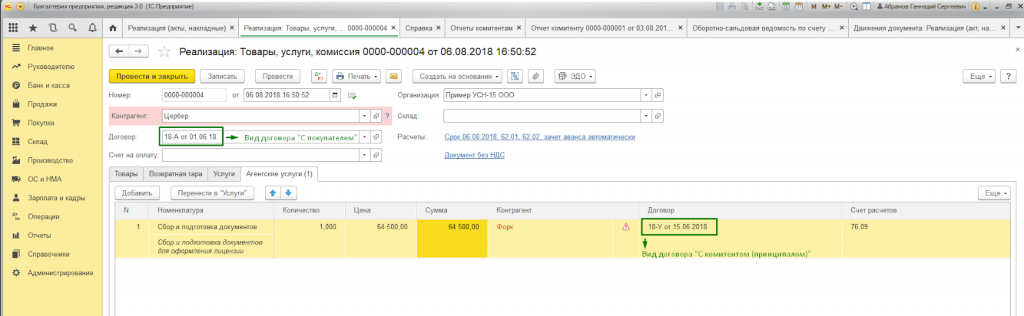

Example 2. An agency agreement was concluded between Primer USN-15 LLC and FORK LLC for services for the collection and preparation of documents for obtaining a security license on its own behalf. This provides for a remuneration for the agent - 10% of the price of services provided, which is calculated from the received DS from buyers.

To display settlements with the buyer with the participation of an agent, the document is drawn up in the same way as in Example 1, but we also fill in “Agency services”.

The settlement account is located automatically, and postings are generated when posting the document.

Upon completion of the services, our company must give the principal a report on the transactions. To do this, and to display the commission, we will create a “Report to the Principal”.

Example 3. LLC "Trading House "Complex" provides service center services for equipment repair.

If we need to reflect the performance of a one-time service or a list of works for an individual order of the buyer without shipping goods, we can use the “Services (Act)” transaction type. We look for the type of operation required in the “Create” submenu.

The tabular part indicates the list of works, and if the service is one-time in nature, you can, without filling out the “Nomenclature” directory, enter a description of the work performed manually.

When posting a document, postings are generated.

A distinctive feature in 1C:Enterprise 8.3 is the presence of the “Provision of Services” document, with the help of which services of a mass nature with a specified frequency are quickly and accurately executed. These services include:

- Service cards in fitness centers (annually);

- Subscriber service for accounting (quarterly);

- Rent in business and shopping centers (monthly);

- IT infrastructure maintenance services (monthly);

- Communication services (monthly), etc.

Thus, the provision of services in 1C 8.3 can be carried out with one document to an unlimited number of clients whose agreement is tied to a specific type of payment.

Example 4. Primer USN-15 LLC provides IT infrastructure maintenance services. Subscriber service agreements have been concluded with a number of clients at a 24/7 tariff costing RUB 25,000/month.

First of all, you need to check the possibility of batch issuing acts and invoices in the program functionality settings on the “Trade” tab (Main - Settings - Functionality).

Also, when drawing up an agreement with the buyer, it is necessary to fill in the “Type of settlements”* in the “Additional information” block.

*Type of calculations – reference book (text line), which is filled in by program users independently, depending on the required grouping of buyer contracts.

To formalize the mass provision of services, we use the “Provision of Services” document, which can be accessed through the “Main Menu – Sales”.

In the document header, you must select from reference books of the same name:

- Nomenclature.

The “Nomenclature” field is necessary to fill in the name of services in the work completion certificate. Moreover, if the “Frequency of service” attribute is set in the “Nomenclature” directory, then the printed form of the act will automatically set the period for which the document is generated.

Thus, there is no need to enter several elements of the “Nomenclature” directory for different periods (rent May 2018, rent June 2018, etc.) or manually adjust the printed form.

The “Fill in by calculation type” button automatically fills in the tabular part of the document.

The “Counterparties” tab (list) displays all buyers whose contract contains the “Type of settlement” attribute specified in the header of the document.

On the “Invoices” tab, the list indicates clients to whom, under the terms of the contract, we provide an invoice for work performed, regardless of the taxation system used by our organization. When posting, the “Invoice issued” document is generated automatically.

Document movements reflect accounting and tax accounting entries, as well as filling out the accumulation register “Sales of services”.

A printed form of the document is generated for each buyer reflected in the document. Numbering is set automatically.

Accounting for the provision of services in 1C 8.3 using any method of registration will lead to the correct generation of accounting and tax reporting. The choice of document form is not regulated, but is chosen by the user based on the convenience of filling out and processing documents.

The 1C manuals describe in some detail how to arrange agency services for the sale of goods (commission trading). We will look at how to arrange agency services for the purchase of goods (services) from the point of view of BP 3.0. In our example, an organization using the simplified tax system leases premises (main activity), has an agreement with energy sales and pays electricity bills. Let's see how to process reimbursement of expenses to the tenant and not lose VAT, because our tenant is on the OSN. The problem is solved in four steps.

First. First of all, you should configure the program. If your database contains only organizations with the accounting policy "USN", then VAT reports are not available to you. In this case, you should add a new organization and assign it "OSN" in the accounting policy. Now on the “Accounting, taxes, reporting” tab you should see the “VAT” group

Second. Next, we will process the receipt of goods (services). We do everything as usual, on the “Purchases” tab, open the “Receipt of goods and services” journal and fill out a new receipt document. In previous releases of the program, this document had only one screen form, but now we have two simplified ones and one full one. We will need type of transaction "Goods, services, commission". It has a tab "Agent services", in the tabular part of which has the columns “Committent” and “Committent Agreement” We select in them the organization for which we will reissue the invoice.

Third. We have already completed the agency purchase itself.Please note that on the “additional” tab you need to fill in the “Consignor” field and save the document.Now we will need a report to the principal in order to draw up an act and re-issue the invoice. It is drawn up on the "Purchases, Sales"\"Reports to Consignors" tab. Here you need to create a new “Purchasing Report”. You only need to select a counterparty, and on the “goods and services” tab there is a “fill in” button. If you have done everything correctly up to this point, the tabular parts of the report will be filled in. This document has a printed report form and an invoice.

Fourth.Finally, we will issue an invoice. In the document “Report to the committent”, the “Print” button provides access to the forms of an invoice and a universal transfer document. After registering the document "Invoice issued". The program has filled out all the data in the invoice, save the document and can print it. Now we can look at the report on the invoice journal. Both parts are filled in.

The question was closed in six mouse clicks.

In the case where goods (works, services) are purchased on behalf of an agent, the following rules must be observed:

-The invoice is issued by the agent in 2 copies on its own behalf. In this case, the number indicated in the invoice is assigned by the agent in accordance with the chronology of invoices issued by him. One copy of this document is handed over to the buyer, and the second is filed in the journal of issued invoices without registering it in the sales book;

The principal must issue the same invoice in the name of the intermediary (agent) with numbering in accordance with the chronology of the invoices issued by him. Moreover, this invoice is not registered in the purchase book of the intermediary (agent).

The procedure for issuing and receiving invoices by an agent for intermediary operations is regulated by the Rules for maintaining logs of received and issued invoices, purchase books and sales books for value added tax calculations, approved by a resolution of the Government of the Russian Federation dated 02.12.2000 No. 914.

When do intermediaries submit VAT returns using the simplified tax system?

As a general rule, “simplified” intermediaries do not pay VAT to the budget and do not file a return for this tax. But at the same time, they reissue invoices for the amount of goods (works, services) sold or purchased for the principal, highlighting the amount of VAT in it (clause 2 of Article 346.11 and clause 1 of Article 169 of the Tax Code of the Russian Federation). They also keep a log of these invoices (Clause 1, Article 12 of Law No. 134-FZ).

But there is an exception to this rule. In the event that intermediaries act as tax agents and buy goods (work, services) from foreign companies, they pay VAT and file a declaration for this tax (clause 5 of Article 161 of the Tax Code of the Russian Federation). Until January 1, 2015, they can submit a VAT return on paper. After this date, the document will be accepted only in electronic form (subparagraph “a”, paragraph 2 of Article 12 and paragraphs 3 and 5 of Article 24 of Law No. 134-FZ).

In trading activities, enterprises use the services of intermediaries. Intermediary operations must be formalized by appropriate agreements, which are divided into: agency agreement, commission agreement and agency agreement.

In accordance with Ch. 52 of the Civil Code of the Russian Federation, under an agency agreement, one party (agent) undertakes, for a fee, to perform, on behalf of the other party, the principal (principal), legal and other actions on its own behalf, but at the expense of the principal, or on behalf and at the expense of the principal.

Let's look at an example. The organization (Agent) entered into an agency agreement with the principal to provide services on its own behalf. The agency fee is 5% of the cost of services sold and is deducted from funds transferred by buyers.

To be able to reflect agency transactions in the 1C Accounting 8 edition 3.0 program, you need to configure the program. Why, in the Program Functionality on the “Trade” tab, enable the necessary items by checkboxes. In our case, this is the sale of goods or services of principals (principals) (Fig. 1)

Picture 1.

To implement the above example in the program, we will need the following documents:

1. Implementation (Act, invoice).

2. Report to the committent.

In the “Sales” section, we will create a Sales document (Act, invoice) with the type of operation “Goods, services, commission”. In the “Head” of the document, fill in the details of the Counterparty and the contract - the type of contract “With the buyer”. In the tabular part on the “Agency services” tab we will indicate the nomenclature - the service, its cost, and the VAT rate. In the counterparty and agreement field, we indicate the principal and the agency agreement (The type of agreement should be “With the principal (principal) for sale”). The contract can specify the option for calculating the agency fee. The settlement account is automatically set to 76.09 “Settlements with various debtors and creditors.” Let's review the document. We will issue an invoice (Fig. 2).

Figure 2.

If the agent sells goods (work, services) of the principal on his own behalf, then the invoice is issued by the intermediary in 2 copies on his own behalf. One copy of this document is handed over to the buyer, and the second is filed in the journal of issued invoices without registering it in the sales book.

After the sale of services, the agent must submit a transaction report to the principal. To perform this operation, as well as to reflect the commission, we need to create a document Report to the Principal, which is located in the “Purchases” section. On the “Home” tab, select the principal and the agency agreement. The commission calculation method will be entered automatically because... We initially specified it in the contract. It is necessary to create the “Remuneration” service; accounting accounts will be automatically filled based on the “Item Accounting Accounts” register. On the goods and services tab, fill out the tabular part using the “Fill in - Fill in sold under the contract” button. We will issue an invoice for the remuneration and look at the document entries. We see that our revenue has been reflected and VAT has been charged. The document settings are shown in (Fig. 3).

Figure 3.

Upon receipt of the report from the agent, the principal must issue invoices for each buyer. The agent must receive a copy of the invoices and register them in the journal of received and issued invoices by the date of receipt.

Invoices received from the principal are created on the basis of a report to the principal. In the invoice document received, you must indicate the number and date, and in the invoice issued to buyers field, select the invoice issued by the agent to the buyer upon sale. (Fig. 4)

Figure 4.

Now we need to generate reports and make sure that our actions are correct. In the “Reports” section we will create a Journal of received and issued invoices (Fig. 5) and a sales book (Fig. 6).

Figure 5.

Recently, a form of doing business has become widespread, when one party carries out any actions on its own behalf (sale of services, sale of goods), but at the expense of the other party, or on behalf and at the expense of the second party, while the first party to such an agreement receives a certain remuneration for his intermediary services. In simple terms, when a performer undertakes to perform certain actions for a customer, receiving material benefits from this. This type of action occurs within the framework of an agency agreement. What such an agreement is and what are the features of accounting and tax accounting - this article will tell you more about this.

Payment order

Relations between two parties bound by an agency agreement are regulated by Chapter 52 of the Civil Code of the Russian Federation. Article No. 1005 of the Civil Code of the Russian Federation defines such relations:

The procedure for paying commissions is determined by Article 1006 of the Civil Code of the Russian Federation:

To calculate the amount of profit due to the contractor, three methods can be used:

- Agency fee expressed as a percentage of the total amount of services or goods sold.

- Agency fee, expressed as a percentage of the difference between the cost of selling goods or providing services and the cost upon receipt.

- Fixed agent fee.

According to Article 997 of the Civil Code of the Russian Federation, depending on the payment procedure approved by agreement between the agent and the customer (hereinafter referred to as the principal), the commission for intermediary services can be transferred (paid) after the invoice is provided or deducted independently from the total amount, payable to the principal. For example, under a contract one party undertakes obligations to sell goods worth one hundred thousand rubles. For executing an order, the intermediary's commission will be 5%. Your 5000 rubles. the agent receives according to the order that was originally prescribed in the contract. If the agreement of the parties provides for the payment of amounts due to the contractor after the report on the work done is approved, the agent will receive his 5% through payment (transfer) by the customer party after the fulfillment of contractual obligations. If the contract provides for a procedure for the intermediary to withhold amounts due to him, then after fulfilling his obligations, the agent sends the amount to the principal minus his own commission.

An agency agreement refers to contracts of a civil law nature. There are a number of points that must be spelled out in such a document:

- the subject of the contract, that is, what exactly the agent must perform, regardless of whether we are talking about the sale of any goods or the provision of all kinds of services;

- names of the parties, details;

- determination of the powers of the performer, that is, an indication on whose behalf the intermediary will carry out the agreed activities;

- validity period (for a certain period or indefinitely);

- reporting procedure;

- the payment procedure together with the amount of the fee due;

- the procedure for limiting the rights of both parties or one of the parties to the contract;

- procedure for terminating the agreement;

- force majeure;

- procedure for considering controversial issues;

- liability of the parties;

- signatures.

Such a document is considered to come into force after it is mutually signed by the parties.

Accounting and tax accounting for an agent

The accounting of the parties will differ, or rather, the accounting entries of the agent will differ from the form of entry that is provided for the principal. According to clause 1, art. 146 of the Tax Code of the Russian Federation, the contractual obligations of an intermediary are subject to value added tax; more precisely, not the actions themselves, but the amount of profit that the performer receives after performing the actions specified in the contract. That is, considering the example given above, where the contractor provided services by selling goods with a total value of one hundred thousand rubles for a fee of 5%, it becomes obvious that this particular percentage is subject to VAT taxation.

As for income tax, according to Art. 249 of the Tax Code of the Russian Federation, the agent’s profit will be considered income received for the provision of services or the sale of goods after deducting tax expenses charged to the principal.

Important! To eliminate possible misunderstandings regarding the fact that the object of taxation is only agency fees, you should be extremely careful about the preparation of documentation at the stage of concluding a contract.

This is what the step-by-step accounting entries for the executor’s side will look like:

Features of accounting for the principal

Due to the fact that the contractor’s side provides only intermediary services, the principal’s subject to VAT taxation will be the full cost of goods or services performed. It should be noted that for the calculation of VAT, the earliest date relative to the choice of the date of shipment or the date of actual payment for services in full or in part will be used in accordance with clause 1, article 167 of the Tax Code of the Russian Federation. That is, if the intermediary receives an advance payment before the seller delivers the goods, VAT will be charged on the amount received in advance. This is what the entries will look like, demonstrating the accounting of agency fees in the principal’s accounting department:

When maintaining accounting records, the principal can reflect the income received only taking into account the submission by the contractor of reports on the results of the work done in accordance with the concluded contract. One of the documents confirming the fact of compliance with the terms of the agreement by the intermediary party is an invoice.

Invoice

An important document for calculating VAT within the framework of cooperation under contracts of this kind is an invoice. Unlike the contract itself, an invoice has a certain established form. There are important features that must be taken into account when issuing an invoice for transactions within the framework of the concluded contract. How and when an invoice is issued for various forms of interaction between the parties to an agency agreement is shown in the table in the photo:

In order for the algorithm for making accounting entries in the 1C program to become more understandable, it is recommended to watch the video instructions, which clearly highlight this point:

Post Views: 573

Edition 8.3 involves working with several documents that are related to each other. “Commissioner's (Agent's) Sales Report” is one of them. Let us explain who a commission agent (agent) is - this is an organization that another organization (committent) has instructed to sell a certain product for a fee. Let us consider in detail how to correctly reflect in the 1C program the entire registration process on behalf of the principal. It is very important to follow the procedure for registering documents:

Transfer of goods to commission (agent).

Receipt of payment from the commission agent (agent) for the goods sold.

Return of unsold goods.

Let's look at each point in order. Initially, you need to correctly draw up an agent agreement in 1C. Please pay attention to the fields:

Type of contract - it is important to indicate the correct type - “With a commission agent (agent) for sale.” The filling of subsequent documents depends on your choice. Price type – select from the directory at what price category the goods will be transferred to the agent. Payment method – here you need to indicate your preferred method of calculating remuneration for the service. For example, select “Percentage of sales amount” from the drop-down list. Amount - indicates how much percentage of the total revenue for the sold goods the agent will receive.

The transfer of goods to the agent is carried out according to the document “Sales: Goods, services, commission”. No invoice is required here:

If you look at the movement of the sales document, you can see that there is no VAT posting. This is influenced by the type of contract chosen. There is only a posting for the transfer of products to the commission at cost: Debit 45.01 Credit 43.

The next step is to prepare the document “Report of the commission agent (agent) on sales.” This can be done directly from the implementation via the “Create” button. The document form has several tabs, consider

Each:

The “Main” tab reflects the basic information on calculations; the document is filled out automatically according to the basis (implementation) document. We check the data in the fields:

Counterparty

Agreement

Calculation method

Calculations:

For goods on invoice 62.01 or 62.02.

For remuneration 60.01 or 60.02.

The compensation expense account should be 44.01

The cost item is commission services (or agent services).

Invoice for remuneration - register.

Please note that if there is a checkmark next to the item “Commission deducted from revenue”, then the agent will make the payment with the deduction of the commission amount.

The Implementation tab contains two sections. The top one displays information about the buyer of the product - the name of the organization, and also, if an invoice was issued, then a tick is placed in the “Invoice” column and the number and date of the document are indicated. The lower field displays a list of sold goods.

The “Returns” tab is filled in if not all goods are sold.

The “Cash” tab contains information about payment from the final buyer and the amount of products sold:

The sales report is completed. Press the “Post and Close” button and look at the transactions that have been generated:

Debit 90.02.1 Credit 45.02 – sales of shipped goods;

Debit 60.01 Credit 62.01 – commission deducted;

Debit 62.01 Credit 90.01.1 – sale of goods;

Debit 44.01 Credit 60.01 – commission costs;

Debit 90.03 Credit 68.02 – VAT on goods;

Debit 19.04 Credit 60.01 – VAT on remuneration.

Payment from the agent for the goods can be received by bank transfer or in cash. It is registered in 1C as a payment receipt document directly from the sales report using the “Create” button. The agent pays the amount minus the remuneration (according to the payment method specified in the contract).

You can reconcile settlements with the agent using the balance sheet, indicating account 62.01:

If you look at the “Sales Book” report, you can see how the goods were sold (through an agent) and to whom (the buyer), as well as the date and number of the seller’s invoice:

The sales book is filled out according to the entered data on the commission agent’s report.

- The organization was created at the end of the year

- Export: VAT refund, zero rate confirmation Zero rate not confirmed 1c

- How to create a children's corner in a children's library: recommendations, exchange of experience Reader's corner in a children's library

- Dalek scientist. Doctor Who and the Daleks. Creation and entry into popular culture

- What is laughing gas: nitrous oxide

- Fundamentals of Theoretical Electrical Engineering for Beginners

- Tragedy turned triumph

- How much does the altruism of the rich cost?

- “So that you do not know grief and luck”

- Morning prayer for good luck Morning prayer for good luck in business

- Morning prayers for good luck Strong morning prayer for good luck in everything

- Advance report: what can be taken into account

- Advance posting report in 1s 8

- Filling out and sample advance report

- personal income tax: example of filling out vacation payments

- How to reflect December vacation pay in 6 personal income taxes

- Features of VAT calculation by tax agents

- Accounting with the principal in 1s 8

- State registration of the issue of shares Information on state registration of the issue of shares

- How to make offsets in 1C Accounting 8.3. Accounting info. Document “Debt Adjustment”