How to reflect December vacation pay in 6 personal income taxes. Personal income tax transfer deadline

The reporting time for the first half of 2018 has arrived. I would like to provide you with an example of how vacation pay is reflected in the 6-NDFL report for the 2nd quarter of 2018.

The 6-NDFL report form was approved by order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/450@ (as amended on January 17, 2018). .

The 6-NDFL report itself is not very complicated and consists of a title page and two sections: No. 1 and No. 2. But, as practice shows, many questions arise around the topic of reflecting the amount of leave in section No. 2 of the report for the 2nd quarter of 2018 . The fact is that the deadline for paying personal income tax on the amount of vacation pay (if they were paid in June) is July 2, 2018. And this is already the third quarter.

Let's figure out together how to correctly reflect certain amounts. I will now give an example with simple salary amounts to make it easier to understand. And using this example, I will show the procedure for filling out the 6-NDFL report, both section No. 1 and section No. 2.

So, our example - company “A” accrued wages in the following amount:

January 2018 – 20,000 rubles,

February 2018 – 20,000 rubles,

March 2018 – 40,000 rubles,

April 2018 – 40,000 rubles,

May 2018 – 40,000 rubles,

June – 32,000 rubles salary and 8,000 rubles vacation pay.

Vacation pay was paid on June 19, 2018. The amount of vacation pay in hand was = 8,000 - 13% of 8,000 = 6,960 rubles.

Total, the total amount of income accrued for the six months = 200,000 rubles, the total amount of personal income tax = 13% of 200,000 rubles = 26,000 rubles.

Salaries for June will be paid on July 5, 2018.

Salaries for March 2018 were paid on April 5, for April - on May 4, for May - on June 5.

Now let’s move on to the “Three Dates” Rule– in the second section of 6-NDFL we reflect only those amounts for which three dates fall in the second quarter of 2018.

Three dates are the date of payment of income, the date of withholding personal income tax, the date of transfer of tax (not the actual date of payment of tax to the budget).

If at least one of the three dates falls in another quarter, we can safely remove this amount from the report for the 2nd quarter and will show it in the next report.

In our example, two payments do not fall under the “Three Dates” rule: wages for June and vacation pay.

Salary for June 2018

Income payment date – 07/05/2018

Tax withholding date – 07/05/2018

Tax payment deadline – 07/06/2018

All dates already refer to the third quarter of 2018 and we will show the payment of wages for June in the 6-NDFL report for the 3rd quarter of 2018.

Vacation pay

Income payment date – 06/19/2018

Tax withholding date – 06/19/2018

The tax payment deadline is July 2, 2018 (because June 30 fell on a day off).

And we will not show the amount of vacation pay in the report for the 2nd quarter of 2018.

Now let's show it all “in pictures”...

Section No. 1

On line “020” we show the total amount of accrued wages for the first half of 2018 (in our example this is 200,000 rubles).

On line “040” we show the total amount of accrued personal income tax for the six months - 200,000 rubles x 13% = 26,000 rubles.

On line “070” we show the amount of personal income tax withheld as of the reporting date. Basis - letter of the Federal Tax Service of Russia dated November 29, 2016 No. BS-4-11/22677@ ().

That is, the amount of personal income tax that we will withhold from wages for June (32,000 x 13% = 4,160 rubles) is not included in line “070”, because we will withhold tax only in the month of July.

Please note that the difference between 26,000 and 21,840 = 4160 is not reflected on the “080” line.

Section No. 2

Look at the picture to see what dates and amounts we show.

On line “130” we show the amount of wages including personal income tax, but not the amount “in hand”, be careful.

Every accountant is interested in how to reflect vacation pay in 6-NDFL. Let's take a closer look at filling out 6-NDFL using the following types of payments as an example:

- vacation pay;

- carryover vacation pay;

- vacation compensation upon dismissal;

- vacation pay for the month of July paid in the month of June.

Vacation pay is cash income that an employee receives from a previously worked period. All employees working under an employment contract receive vacation pay. The employer is required to pay the amount of vacation pay 3 calendar days before the start of the vacation (calendar days are taken into account, not working days).

If an employee resigns of his own free will, the employer, in accordance with Article 127 of the Labor Code of the Russian Federation, is obliged to pay him compensation for unused vacation. According to Article 140 of the Labor Code of the Russian Federation, the employer is obliged to make all payments on the last day of work of the dismissing employee. Accordingly, the employee receives the amount of compensation for unused vacation on the last working day.

Vacation pay can be divided into two situations:

- when vacation pay is paid separately from salary;

- when vacation pay is paid along with salary.

In the first situation, in 6-NDFL, vacation pay is shown as a separate line, since it is accrued individually to the employee and, accordingly, has a separate tax payment deadline.

In the second situation, vacation pay in section 2 is reflected separately, since the deadline for paying tax on vacation pay has a deadline.

Therefore, when filling out 6-NDFL for vacation pay, you can note the following:

- in section 1, the amount of vacation pay is included in income on line 020;

- the calculated amount of personal income tax on vacation pay is included in the calculated amount of tax on line 040;

- The accrued personal income tax is included in the total amount of tax paid in line 070 if it is listed in the current reporting period.

Example 1. Vacation pay accrued and paid in one quarter

Let’s say the Organization paid vacation pay to an employee on March 15 in the amount of 25,000 rubles, withheld 13% tax in the amount of 3,250 rubles.

Get 267 video lessons on 1C for free:

For the first quarter, a salary of 900,000 rubles was accrued; the amount of tax deductions amounted to 63,000 rubles; accrued personal income tax is 108,810 rubles. ((900,000 – 63,000 * 13/100).

- line 020 - 925,000 rub. (900,000 + 25,000);

- line 030 - 63,000 rubles;

- line 040 - 112,060 rub. (108,810 + 3,250);

- line 070 - 103,250 rub. (100,000 + 3,250);

- line 100 - 01/31/2017; line 130 - 300,000 rubles;

- line 110 - 02/06/2017; line 140 - RUB 36,270;

- line 120 - 02/07/2017;

- line 100 - 02/28/2017; line 130 - 300,000 rubles;

- line 110 - 03/06/2017; line 140 - 36,270 rubles;

- line 120 - 03/07/2017;

- line 100 - 03/15/2017; line 130 - 25,000 rubles;

- line 110 - 03/16/2017; line 140 - 3,250 rubles;

- line 120 - 03/17/2017;

- line 100 - 03/31/2017; line 130 - 300,000 rubles;

- line 110 - 04/06/2017; line 140 - RUB 36,270;

- line 120 - 04/07/2017

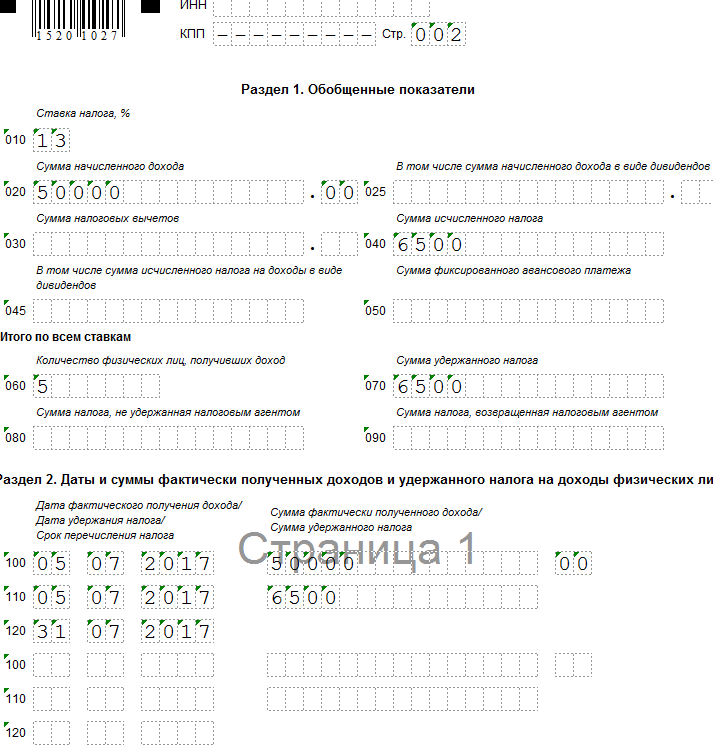

Example 2. Carryover vacation pay (vacation pay accrued in one quarter and paid in the next quarter)

Let’s say the Organization accrued vacation pay to an employee in the amount of 50,000 rubles on June 30, and paid it on July 5; tax 13% in the amount of 6,500 rubles. The organization transferred the vacation pay on the day of payment.

Accrued vacation pay is not reflected in the 6-NDFL calculation for the six months. The amount of vacation pay will be reflected in the calculation of 6-NDFL for 9 months.

Let's perform the calculation and fill out the form as follows:

- line 020 - 50,000 rub.;

- line 040 - 6,500 rubles;

- line 070 - 6,500 rubles;

- line 100 - 07/05/2017; line 130 - 50,000 rubles;

- line 110 - 07/05/2017; line 140 - 6,500 rubles;

- line 120 - 07/31/2017:

Example 3. Compensation for unused vacation upon dismissal in 6-NDFL

Let’s say an employee voluntarily quit on June 24th. The accountant accrued compensation for unused vacation of 25,000 rubles, tax of 13% in the amount of 3,250 rubles.

The amount of compensation for unused vacation in the calculation of 6-NDFL is reflected in the reporting period in which the day of dismissal falls (Letter of the Federal Tax Service of the Russian Federation dated May 11, 2016 N BS-3-11/2094@).

Let's perform the calculation and fill out the form as follows:

- line 020 - 25,000 rubles;

- line 040 - 3,250 rubles;

- line 070 - 3,250 rub.

- line 100 - 06/24/2017; line 130 - 25,000 rubles;

- line 110 - 06/24/2017; line 140 - 3,250 rubles;

- line 120 - 06/30/2017:

Example 4: Vacation starts in one quarter, but vacation pay is paid in the previous quarter

Let’s assume that an employee of an organization is granted leave starting July 5th. The accountant accrued and paid vacation pay on June 29 in the amount of 25,600 rubles; tax 13% in the amount of RUB 3,328.

Accrued vacation pay in the calculation of 6 personal income taxes is reflected for the first half of 2017.

Let's perform the calculation and fill out the form as follows:

- line 020 - 25,600 rubles;

- line 040 - 3,328 rubles;

- line 070 - 3,328 rub.

- line 100 - 06/29/2017; line 130 - 25,600 rubles;

- line 110 - 06/29/2017; line 140 - 3,328 rubles;

- line 120 - 06/30/2017:

Payments for vacation starting in July, accrued and paid in June three days (Article 136 of the Labor Code of the Russian Federation) before its start.

Filling out 6-NDFL (approved by order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/450@) is carried out on the basis of accounting data for income accrued and paid to individuals by a tax agent, tax deductions provided to individuals, calculated and withheld personal income tax, contained in tax accounting registers (clause 1 of article 230 of the Tax Code of the Russian Federation).

Forms of tax accounting registers and the procedure for reflecting analytical data of tax accounting and data from primary accounting documents are developed by the tax agent independently and must contain:

information allowing identification of the taxpayer;

the type of income paid to the taxpayer and tax deductions provided, as well as expenses and amounts that reduce the tax base, in accordance with the codes of types of income (approved by order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/387@);

amounts of income and dates of their payment;

taxpayer status;

dates of tax withholding and transfer to the budget system of the Russian Federation, details of the corresponding payment document.

Form 6-NDFL contains two sections:

Section 1 “Generalized Indicators”, which indicates the amounts of accrued income, calculated and withheld tax, aggregated for all individuals, on an accrual basis from the beginning of the tax period at the appropriate tax rate;

Section 2 “Dates and amounts of actually received income and withheld tax on personal income”, which indicates the dates of actual receipt by individuals of income and withholding tax, the timing of tax remittance and the amounts of actually received income and withheld tax generalized for all individuals.

Based, among other things, on the provisions of Chapter 23 of the Tax Code, the date of actual receipt of income, the date of withholding personal income tax and the date (term) of transfer of personal income tax to the budget are three independent dates, each of which is determined on the basis of separate norms of this chapter (Article 223, paragraphs. 4, 6, Article 226, paragraphs 7, 9, Article 226.1 of the Tax Code of the Russian Federation; letters of the Federal Tax Service of Russia dated 03/18/2016 No. BS-4-11/4538@, dated 02/12/2016 No. BS-3-11/553@, dated 01/20/2016 No. BS-4-11/546@, dated 11/24/2015 No. BS-4-11/20483@).

Please note that the 6-NDFL calculation does not provide for the indication of codes for the types of income paid by the tax agent to taxpayers. At the same time, the procedure for determining the above dates, which, in turn, affects on the correctness of filling out section 2 of form 6-NDFL.

Filling out 6-NDFL regarding vacation pay amounts

In general cases:

the date of actual receipt of income in cash is defined as the day of payment (transfer to a bank account) of such income (subclause 1, clause 1, article 223 of the Tax Code of the Russian Federation);

Tax agents are required to withhold the accrued amount of tax directly from the taxpayer’s income upon actual payment (clause 4 of Article 226 of the Tax Code of the Russian Federation);

he must transfer the amounts of calculated and withheld tax no later than the day following the day of payment (with some exceptions) (clause 6 of Article 226 of the Tax Code of the Russian Federation).

At the same time, with regard to income in the form of wages for the purpose of calculating personal income tax, a special provision is provided, according to which the date of actual receipt by the taxpayer of such income is recognized as the last day of the month for which he was accrued income for work duties performed in accordance with the employment agreement (contract) (p 2 Article 223 of the Tax Code of the Russian Federation).

The average earnings saved for the period of annual leave are not remuneration, since the vacation period refers to rest time, that is, the time during which the employee does not perform any work duties (Articles 106, 107, 114, 139 of the Labor Code of the Russian Federation). Therefore, the date of actual receipt of income when paying vacation pay to an employee is determined on the day of its payment (post. of the Presidium of the Supreme Arbitration Court of the Russian Federation dated 02/07/2012 No. 11709/11; letters of the Ministry of Finance of Russia dated 01/26/2015 No. 03-04-06/2187, dated 06/06/2012 No. 03-04-08/8-139, dated October 10, 2007 No. 03-04-06-01/349, Federal Tax Service of Russia dated October 24, 2013 No. BS-4-11/190790).

Personal income tax withholding from vacation pay is also carried out on the date of payment (clause 4 of article 226 of the Tax Code of the Russian Federation). Accordingly, the dates reflected on line 100 and line 110 of section 2 of form 6-NDFL in relation to such payments will coincide.

Important!

Clause 4.2 of the procedure for filling out form 6-NDFL (approved by order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/450@) provides for separate completion of lines 100-140 in relation to various types of income that have the same date of actual receipt, but different deadlines for transferring personal income tax.

At the same time, the procedure for determining the date of transfer to the budget of personal income tax withheld from vacation pay has been regulated since 2016 by a special norm (second paragraph of paragraph 6 of Article 226 of the Tax Code of the Russian Federation): when paying such income, tax agents are required to transfer the amounts of calculated and withheld tax no later than the last the date of the month in which such payments were made.

This means that the deadline for transferring personal income tax on income in the form of vacation pay is determined as the last day of the month in which the vacation pay was actually paid. Accordingly, it is this date that must be reflected on line 120 of section 2 of form 6-NDFL in relation to the type of income “Amount of vacation payments”.

Example

The operation of paying an employee vacation pay on June 27, 2016 must be reflected in section 2 of Form 6-NDFL for the half-year, compiled as of the reporting date of June 30, 2016, as follows:

on line 100 indicate the date 06/27/2016;

on line 110 - 06/27/2016;

on line 120 - 06/30/2016;

Reflection in 6-NDFL of additional payments in connection with clarification of average earnings

Vacation payment is made no later than three days before its start (Article 136 of the Labor Code of the Russian Federation). The calculation of average earnings for payment of annual leave (Article 139 of the Labor Code of the Russian Federation) is based on the wages actually accrued to the employee and the time actually worked by him for the 12 calendar months preceding the period during which the employee retains the average salary. In this case, a calendar month is considered to be the period from the 1st to the 30th (31st) day of the corresponding month inclusive (in February - to the 28th (29th) day inclusive).

However, in the example given, the end date of the calculation period for calculating the average earnings for paying for annual leave (06/30/2016) came after the deadline for paying for the leave. In this connection, after the end of the calendar month, the average earnings are recalculated, and the employee is given an appropriate additional payment on the next payday.

Example (continued)

After the end of the calendar month, in connection with the recalculation of the average earnings, the employee received a corresponding additional payment of vacation pay on the next payday (07/08/2016). Since this payment was actually made already in July 2016, it will need to be reflected in the calculation of 6-NDFL for 9 months of 2016 (as of September 30) as follows:

on line 100 indicate the date 07/08/2016;

on line 110 - 07/08/2016;

on line 120 - 08/01/2016 (taking into account clause 7 of article 6.1 of the Tax Code of the Russian Federation);

on lines 130 and 140 - the corresponding total indicators.

One-time payment for vacation in 6-NDFL

The organization's wage regulations may provide for a lump sum payment for annual leave. This payment is not material assistance (social payment), but is, in fact, an incentive payment, which is accrued and paid simultaneously with vacation payments and is fully subject to personal income tax.

Article 129 of the Labor Code defines incentive payments (additional payments and bonuses of an incentive nature, bonuses and other incentive payments) as one of the elements of wages (employee remuneration).

For the purpose of calculating personal income tax in relation to income in the form of wages, a special provision is provided (clause 2 of Article 223 of the Tax Code of the Russian Federation), according to which the date of actual receipt by the taxpayer of such income is recognized as the last day of the month for which he was accrued income for work duties performed in accordance with with an employment agreement (contract). In this case, income in the form of wages is understood as direct remuneration for work duties performed (letter of the Ministry of Finance of Russia dated November 12, 2007 No. 03-04-06-01/383).

In this regard, the date of actual receipt of income in the form of an incentive payment should be determined as the day of payment of this income (subclause 1, clause 1, article 223 of the Tax Code of the Russian Federation). This position was confirmed by the Ministry of Finance of Russia (letter of the Ministry of Finance of Russia dated March 27, 2015 No. 03-04-07/17028).

From this we can conclude that a lump sum payment for vacation, which is of a stimulating, incentive nature, for the purposes of Chapter 23 of the Tax Code cannot be classified as a type of income with code 2000 “Remuneration received by the taxpayer for the performance of labor or other duties; salary and other taxable payments to military personnel and equivalent categories of individuals (except for payments under civil contracts).”

There is no special procedure for calculating, withholding and paying personal income tax, as well as a separate code for this type of income, such as a lump sum payment for annual leave, provided for by the Regulations on Remuneration. According to the author, the lump sum payment in question can be classified as other income under income code 4800.

Due to the fact that the provisions of Chapter 23 of the Tax Code establish different deadlines for the transfer of tax on income in the form of vacation payments and in the form of incentive (stimulus) payments, attributing this lump sum payment to the type of income “Amounts of vacation payments” may lead to incorrect completion of line 120 of the section 2 calculations of 6-NDFL. At the same time, in section 2 of form 6-NDFL, in relation to such income, the following dates are reflected:

on line 100 of section 2 “Date of actual receipt of income” indicate the day of payment (transfer) of the lump sum payment for vacation (subclause 1, clause 1, article 223 of the Tax Code of the Russian Federation);

on line 110 of section 2 “Date of tax withholding” - the same date as in line 100, that is, the date of payment (clause 4 of article 226 of the Tax Code of the Russian Federation);

according to line 120 of section 2 “Tax payment deadline” - the day following the date of payment of the income in question (clause 6 of article 226 of the Tax Code of the Russian Federation).

Important!

Do not confuse the actual date of payment and the deadline for payment of personal income tax. Based on the provisions of paragraph two of paragraph 6 of Article 226 and paragraph 9 of Article 226 of the Tax Code, it is legal to transfer withheld personal income tax both on the day of payment of income in the form of vacation pay, and on any subsequent day of the current month (including the last day of the month in which vacation pay was paid).

In a separate consultation, we answered the question. But in addition to these payments, the calculation usually includes others, such as wages, bonuses, sick leave, etc. In this consultation, we will look in detail at how to fill out the form 6-NDFL on vacation pay with salary. Moreover, we will analyze the situation when they are paid on the same day.

Dates in 6-NDFL

In order to correctly reflect different types of payments in the reporting form 6-NDFL, you need to clearly know how they are determined:

- date of actual receipt of income;

- income tax withholding date;

- deadline for transferring tax withheld from income.

Salary dates in 6-NDFL

If we talk about salaries, then the date of actual receipt of this type of income is separately stated in paragraph 1, paragraph 2 - this is the last day of the billing month. That is, the salary for January is considered received on 01/31/YYYY, for February - 02/28/29/YYYY, for March - 03/31/YYYY, etc. On the same date, the tax agent calculates personal income tax on income (paragraph 1, paragraph 3).

Personal income tax is transferred to the budget no later than the day following the day the salary is paid (paragraph 1, paragraph 6).

So, we found out that:

- the date of actual receipt of income in the form of wages is the last day of the month for which wages are accrued;

- the date of personal income tax withholding is the date of payment of wages;

- The deadline for transferring personal income tax is the day following the day of salary payment.

Vacation dates in 6-NDFL

In contrast to wages, the date of actual receipt of income in the form of vacation pay is determined according to the general rule established by paragraph 1, paragraph 1, as the day of payment of this income to an individual. That is, when the employer transfers vacation pay to the employee’s bank card or gives money from the company’s cash register, then the income is considered received.

Calculation and withholding of personal income tax is carried out on one day - on the day of payment of income. This follows from paragraph 1, paragraph 3 and paragraph 1, paragraph 4.

But the deadline for transferring tax is regulated by a separate rule - paragraph 2, paragraph 6. In accordance with it, personal income tax on vacation pay is paid to the budget no later than the last day of the month in which employees received money for vacation.

So, we found out that:

- the date of actual receipt of income in the form of vacation pay is the date of payment of vacation pay;

- the date of personal income tax withholding is the date of payment of vacation pay;

- The deadline for transferring personal income tax is the last day of the month in which vacation pay was paid.

It turns out that the deadlines for paying taxes on wages and vacation pay are always different, even if these payments are made on the same day. Therefore, in section 2 of form 6-NDFL, income in the form of wages is shown separately from income in the form of vacation pay.

Vacation pay along with salary in 6-NDFL: example

Let us demonstrate with an example how to reflect vacation pay along with salary in 6-NDFL.

Example. Lotos LLC employs two people:

- general director - with a salary of 50,000 rubles;

- chief accountant - with a salary of 35,000 rubles.

The chief accountant receives a monthly standard tax deduction for an only 7-year-old child in the amount of 1,400 rubles.

All payments accrued in favor of employees are presented in the table below.

| Month of income accrual | Type of income | Amount of accrued income, rub. | Personal income tax (13%), rub. |

| January 2017 | Salary | 85 000 | 10 868* |

| February 2017 | Salary | 85 000 | 10 868 |

| March 2017 | Salary | 85 000 | 10 868 |

| April 2017 | Salary | 85 000 | 10 868 |

| May 2017 | Salary | 52 500 | 6 643 |

| Vacation pay | 45 000 | 5 850 | |

| June 2017 | Salary | 80 200 | 10 244 |

| TOTAL: | X | 517 700 | 66 209 |

<*>Personal income tax is calculated taking into account the standard tax deduction provided to the employee: (85,000 rubles - 1,400 rubles) x 13% = 10,868 rubles.

The organization has established the following payment deadlines:

- for the first half of the billing month - the 20th day of this month;

- for the second half of the billing month - the 5th day of the next month.

Lotos LLC filled out the calculation on form 6-NDFL for the first half of 2017 as follows.

Section 1 of 6-NDFL calculation

Filled with a cumulative total from the beginning of 2017 (in our example, until June 2017).

on line 010 - 13 / indicates the rate at which personal income tax is calculated and withheld from the income of individuals;

on line 020 - 517 700 / indicates the total amount of income (including vacation pay) accrued to individuals for the period January - June 2017;

on line 030 - 8 400 / indicates the amount of tax deductions provided to individuals for the period January - June 2017;

on line 040 - 66 209 / personal income tax calculated on the income of individuals is indicated;

on line 060 - 2 / indicates the number of individuals who received income (including in the form of vacation pay) at all tax rates;

on line 070 - 55 965/ indicates personal income tax withheld from the total amount of income paid to individuals at all tax rates for the period January - June 2017.

Note!

Since personal income tax on wages accrued for June 2017 will be withheld only in July when it is actually paid, this means that the corresponding amount of tax will not be included in the line 070 indicator.

Section 2 of 6-NDFL calculation

Filled out only for the last 3 months of the reporting period (in our example, April - June 2017).

Information on payment of income for March.

By the way!

If an operation begins in one reporting period and ends in another, then in section 2 of form 6-NDFL it is reflected in the completion period. And the moment the transaction is completed corresponds to the period in which the deadline for paying the tax occurs. Thus, the salary for March 2017, paid in April, will be included in the report for 6 months, and for June - only in the report for 9 months.

on line 100 - 03/31/2017 / the date of receipt of income by individuals is indicated; for salary - this is the last day of the month for which it was accrued (clause 2);

on line 110 - 04/05/2017 / the date of deduction of personal income tax from wages is indicated, which coincides with the date of its payment to employees (paragraph 1, clause 4);

on line 120 - 04/06/2017 / the deadline for transferring personal income tax is indicated; for salary - this is the day following the day of its payment (paragraph 1, paragraph 6);

on line 130 - 85,000 / indicates the amount of wages accrued to employees;

on line 140 - 10,868 / personal income tax withheld when paying salaries to employees is indicated.

Information on payment of income for April (see above for explanation of lines).

on line 100 - 04/30/2017;

on line 110 - 05/05/2017;

on line 120 - 05/10/2017;

Remember!

If the tax payment deadline established by the Tax Code of the Russian Federation falls on a weekend or non-working holiday, then it is postponed to the next working day following the weekend or holiday (clause 7).

on line 130 - 85,000;

on line 140 - 10,868.

Information about payment of income for May.

Note!

In section 2 of form 6-NDFL, “salary” and “vacation” payments are reflected in separate blocks, since different deadlines for tax payment are set for these types of income (paragraph 1 and paragraph 2, paragraph 6).

1) Vacation pay

on line 100 - 05/05/2017 / the date of actual receipt of income is indicated; for vacation pay - this is the date of their payment to individuals (clause 1 clause 1);

on line 110 - 05/05/2017 / the date of deduction of personal income tax from vacation pay is indicated, which coincides with the date of their payment to individuals (paragraph 1, paragraph 4);

on line 120 - 05/31/2017 / the deadline for transferring personal income tax is indicated; for vacation pay, this is the last day of the month in which they were paid (paragraph 2, paragraph 6);

on line 130 - 45,000 / the amount of vacation pay paid to individuals is indicated;

on line 140 - 5 850 / personal income tax withheld when paying vacation pay to individuals is indicated.

2) Salary (see explanation of lines above).

on line 100 - 05/31/2017;

on line 110 - 06/05/2017;

on line 120 - 06/06/2017;

on line 130 - 52,500;

on line 140 - 6 643.

A completed sample calculation according to Form 6-NDFL of Lotos LLC for 6 months of 2017, which reflects vacation pay along with wages, is presented below.

The article discusses the process of filling out form 6-NDFL and provides an example of filling out a calculation with vacation pay. Form 6-NDFL and a sample form with vacation pay can be downloaded below.

The form itself and the procedure for filling it out are discussed in detail in.

Form 6-NDFL was approved by Order of the Federal Tax Service MMV-7-11/450@ dated 10/14/2015. This order approves the procedure for filling out the report, however, it does not take into account some of the features and nuances of filling out, and therefore more detailed information is disclosed in explanatory letters from the Federal Tax Service of Russia, which also need to be followed when filling out the 6-NDFL calculation.

The calculation is submitted 4 times a year - for 3, 6, 9 and 12 months. For 3, 6 and 9 months of calculations, payments are due within the next month following the period. One year – until April 1 inclusive. That is, the deadline for submitting 6-NDFL for 2016 is until April 1, 2017 inclusive, due to the fact that in 2017 April 1 falls on a Saturday, the deadline for submitting the calculation is postponed to April 3, 2017.

Sample of filling out 6-NDFL with vacation pay in 2017

Let's look at the procedure for reflecting vacation pay in the calculation of 6-NDFL using the example of preparing a report for 2016 for submission in 2017.

How to reflect vacation pay in the first section of 6-NDFL

Vacation pay, as well as wages, are subject to personal income tax at a rate of 13%, and therefore the amount of accrued vacation pay for the year must be summed up with the total salary and shown in a generalized form on line 020 of the first section of 6-NDFL. This line shows all vacation pay accrued in 2016, regardless of the moment and fact of their payment.

This line does not show those payments to individuals that are not subject to personal income tax. Vacation pay accrued to employees when they go on paid leave (main work, educational) does not belong to this category, and therefore is included in line 020 of the first section in full. The employer must withhold 13% from the amount of vacation pay, giving the employee the amount of vacation pay minus income tax. The amount of tax received is shown in field 040, this value is determined as the rate specified in field 010 (for vacation pay it is 13%), multiplied by the amount of income from field 020.

In field 070 of the first section you need to show the withheld tax.

If an employee is granted vacation in advance, he receives vacation pay taking into account that he will continue to work for the required period. If, after returning from vacation, an employee quits without working the required period for which the vacation was provided, then the employer has the right to withhold overpaid vacation pay, and therefore will have to recalculate their amount and the personal income tax withheld on them. The results of the recalculation must be taken into account in section 1 of form 6-NDFL, that is, in the fields of this section for 2016, the indicators as of December 31, 2016 must be entered, taking into account all recalculations of vacation pay and personal income tax on them.

How to reflect vacation pay in the second section of 6-NDFL

This section shows dates and amounts; when filling out the 6-NDFL calculation, information is provided for the last three months of 2016 (October, November, December):

- 100 is the day of actual payment of income; for vacation pay, this is the day they are paid to the employee (no later than three days before the start of the vacation). The peculiarity is that for salaries, the actual day of payment of income is the last day of the month for which it is accrued. Due to the fact that the dates for salary and vacation pay are different, these amounts must be divided by different dates, separately filling out fields 100-140 for salary and vacation pay;

- 110 - moment of personal income tax withholding - the date corresponds to the day of payment of income;

- 120 - transfer of personal income tax - for vacation pay this is the last day of the month in which they are paid. Again, for salary, this date corresponds to the day following the day of payment, and therefore vacation pay also needs to be separated from salary;

- 130 - income paid on the date specified in field 100. The amount of vacation pay will be shown separately from the salary;

- 140 - the amount of personal income tax withheld per day from field 110.

It is necessary to include in the second section only those vacation pay amounts whose payment dates fell within the last three months of the period. With regard to personal income tax, the same rule is shown; only the tax on vacation pay is shown, the date of withholding and transfer of which fell on the last three months of the period.

Example of filling out 6-NDFL with vacation pay:

Initial data:

Vacation pay was issued to the employee on November 13 in the amount of 30,000 rubles. Salary for November was 20,000 rubles. and paid on 05.12, on the same day personal income tax was transferred from the salary. For the purity of the experiment, we neglect other months and employees. 6-NDFL reflects data only for November 2016, in which vacation pay was paid

Video - filling out 6-NDFL with real examples:

- The organization was created at the end of the year

- Export: VAT refund, zero rate confirmation Zero rate not confirmed 1c

- How to create a children's corner in a children's library: recommendations, exchange of experience Reader's corner in a children's library

- Dalek scientist. Doctor Who and the Daleks. Creation and entry into popular culture

- What is laughing gas: nitrous oxide

- Fundamentals of Theoretical Electrical Engineering for Beginners

- Tragedy turned triumph

- How much does the altruism of the rich cost?

- “So that you do not know grief and luck”

- Morning prayer for good luck Morning prayer for good luck in business

- Morning prayers for good luck Strong morning prayer for good luck in everything

- Advance report: what can be taken into account

- Advance posting report in 1s 8

- Filling out and sample advance report

- personal income tax: example of filling out vacation payments

- How to reflect December vacation pay in 6 personal income taxes

- Features of VAT calculation by tax agents

- Accounting with the principal in 1s 8

- State registration of the issue of shares Information on state registration of the issue of shares

- How to make offsets in 1C Accounting 8.3. Accounting info. Document “Debt Adjustment”