Accounting info. Accounting info Transfer of workwear into operation 1s 8.3

How to take into account special clothing in 1c? How to credit workwear in 1C 8.3? Accounting for workwear and special equipment in 1C: Accounting 8.2 8.3 Part I

Receipt and transfer into operation of workwear and special equipment

We will devote today's article to considering an issue that also periodically arises among users of the 1C program. Namely: “How to write off workwear in 1C? How to take into account special clothing in 1s 8.3? Accounting for workwear in 1C: Accounting 8.2 8.3"

There is nothing supernatural or special about such accounting; nevertheless, the question exists and takes place. How to reflect the receipt of workwear and special equipment, how to write off workwear from service, in what account to account for workwear, how to transfer workwear into operation, how to pay off the cost of workwear and special equipment in accounting and tax accounting - these are the questions that we will also find answers to in today’s lesson .

The topic of workwear is not new. It has been discussed many times and on the Internet you can find many different articles devoted to this topic in 1C 7.7 or 1C 8.2. However, time flows and 1C changes. Today we will work with a relatively new 1C interface, namely the “Taxi” interface, used in 1C version 8.3.

So let's get started.

In the first part of our lesson, we will look at the receipt of workwear and special equipment, as well as the transfer of workwear and special equipment into operation.

Part I

To reflect receipt of workwear We use the document “Receipt of goods and services”. It is located along the following path - being on the main page, click on the item in the right menu “Purchases” and then select “Receipt of goods and services”.

We draw up a new document with the type of operation “Goods”. For the case when, simultaneously with the arrival of workwear, you need to register services, you need to use the “Goods, services, commission” transaction type. So, “Products”.

Fill out the header of the new document. We indicate the number and date, warehouse, counterparty and contract. If the necessary elements are missing, we create a new one. Then we add rows to the table section.

Select the item from the “ ” or “Special equipment” folder, respectively. If groups are not organized, then we create them. This action is not mandatory, but desirable for your own convenience. For example, in the case of preliminary organization and indication of such groups, accounting accounts will be substituted automatically from those previously entered in the groups.

If the product card is not organized, then we also create it. We discussed how to work with the nomenclature directory in the article ““

We indicate the data for the row of the tabular part - price and quantity. Workwear accounting account 10.10, VAT account 19.03.

At the end of creating the document, we indicate and register an invoice (if necessary).

We navigate and close the document.

Next you need transfer workwear or special equipment to production. For this purpose, the document “Transfer of materials into operation” is used. We find it by going to the contents of the “Warehouse” tab. Let's create a new document.

Select the warehouse and organization and click the “Create” button.

The program will automatically fill in the necessary details of the header, but all we have to do is enter the location of the unit in which the MOL is located, to which the protective clothing is issued.

The next step is to enter data into the table section. Add the items required for transfer.

Fill in the quantity and individual.

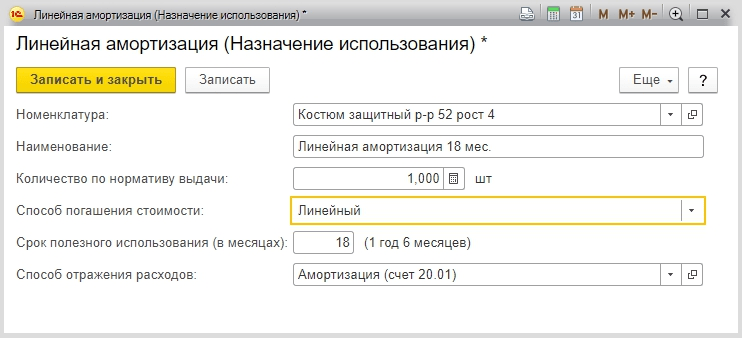

The next item “Purpose of use” will require some additional action from us. This data is used to reflect the method of paying off the cost of workwear or special equipment for expenses. It is mandatory to fill it out.

Let's add a purpose of use by selecting the button built into the tabular part.

It should be noted that workwear that depreciates for 12 months. is accounted for as inventory and is written off simultaneously in both accounting and tax accounting upon transfer to operation. If the useful life exceeds 12 months, then in accounting the workwear will be written off on a straight-line basis depending on the period of use. In tax accounting, workwear is written off as material expenses also when it is put into operation. If the cost of workwear exceeds 40 thousand, then it is taken into account as a fixed asset.

Let's create a new one or select an existing usage purpose.

We fill in the name, in which it is desirable to indicate the features that distinguish this type of intended use; We indicate the quantity according to the issuance standard. In our case it is -1 pc. Next, we introduce a linear cost repayment method for our example. We indicate the period in months and the method of reflecting expenses (20 or 25 accounts).

Swipe and close the document. When posted, the document will generate postings to accounts 10.10 and 10.11, as well as to the debit of the wealth accounting accounts.

If you believe that workwear is issued only to construction workers and factory workers, then take a look at the Standard Standards approved by Order of the Russian Ministry of Labor dated December 09, 2014 No. 997n. Among others, you will see in the list of positions: driver, archivist, computer operator, loader, technician, supply manager, seller of non-food products, which can be in almost any company.

Since the employer is responsible for organizing safe conditions and labor protection, employees must be provided with personal protective equipment. This article will help you organize accounting of workwear in your organization.

1. Standards for providing workers with special clothing

2. Card for free issue of workwear

3. Postings for accounting of workwear

4. Write-off of workwear in accounting

5. Example

6. Write-off of workwear in tax accounting

7. Accounting for workwear in 1s 8.3

8. Accounting for workwear in an organization using the simplified tax system

9. How to write off workwear that has become unusable

10. Overalls when dismissing an employee

So, let's go in order. If you don't have time to read a long article, watch the short video below, from which you will learn all the most important things about the topic of the article.

(if the video is not clear, there is a gear at the bottom of the video, click it and select 720p Quality)

We will discuss the topic further in the article in more detail than in the video.

1. Standards for providing workers with special clothing

To whom the employer is obliged to issue special clothing is specified in Articles 212, 221 of the Labor Code of the Russian Federation:

- workers engaged in work with harmful or dangerous conditions labor;

- workers engaged in work performed in special temperature conditions or those associated with pollution.

The document that regulates the provision of workers with special clothing is the Intersectoral Rules for Providing Workers with Special Clothing, Special Footwear and Other Personal Protective Equipment, approved by Order of the Ministry of Health and Social Development of Russia dated June 1, 2009 No. 290n. It is installed issuance requirements personal protective equipment (PPE):

- PPE must undergo certification and declaration of conformity;

- PPE is purchased at the expense of the organization or under a lease agreement for temporary use;

- PPE is issued free of charge according to standard standards and based on the results of a special assessment of working conditions

- An organization, in a local act, can establish its own standards for providing workers with protective clothing that exceed the standard ones, and also replace one type of protective clothing with a similar level of protection.

You can check the standards for providing workers with special clothing for positions available in the staffing table in following documents:

- Model standards approved by Order of the Ministry of Labor of Russia dated December 9, 2014 No. 997n - for workers in cross-cutting professions and positions of all types of economic activity;

- Standards for issuing warm work clothes and footwear to employees, approved by Resolution of the Ministry of Labor dated December 31, 1997 No. 70 - according to climatic zones, the same for all sectors of the economy;

- Standard issuance standards approved by Order of the Ministry of Health and Social Development dated April 20, 2006 No. 297 - for certified special high-visibility signal clothing to workers in all sectors of the economy;

- Industry standard standards (for example, in construction, medical, manufacturing activities, banks, housing and communal services, etc.).

- in Section IV of the Report on the special assessment of working conditions (Appendix No. 3 to Order of the Ministry of Labor of Russia dated January 24, 2014 N 33n).

In these documents, for each position and profession, you can find a list of special clothing by type and quantity that should be issued to employees for the year.

The enterprise must approve the list of positions to which special clothing is issued and the issuance standards. This may be an order from the manager or an annex to an employment or collective agreement.

Appendix to the order:

When hiring an employee, the employer must inform the employee about the personal protective equipment they are required to wear. The employee signs that he has read the Rules for Providing Workers with Work Clothing and the standard standards for issuing PPE that correspond to his profession and position.

2. Card for free issue of workwear

When issuing workwear to employees, one should take into account the gender, height and size of the employee, and the nature of his work. To control the standards for issuing workwear and their service life, fill out personal card for issuing personal protective equipment for each employee. The form of the card for the free issuance of workwear is approved by the Intersectoral Rules (Order of the Ministry of Health and Social Development of Russia dated June 1, 2009 No. 290n).

Intersectoral rules allow maintaining personal cards in paper or electronic form. When filling out a personal registration card for the issuance of PPE in the program, instead of the employee’s signature on receipt, a reference is made to the details of the primary document, which contains the employee’s signature on receipt of PPE (for example, claim invoice M-11).

If PPE is not used by employees all the time, but is required for the duration of certain work, a card for the free issuance of protective clothing marked “On duty” is issued for them.

When registering operations for the movement of workwear, the accounting department, as a rule, transfers documentation according to unified forms (approved by Resolution of the State Statistics Committee of the Russian Federation dated October 30, 1997 No. 71a):

- No. MB-2 “Registration card for low-value and wear-and-tear items”;

- No. MB-4 “Act of disposal of low-value and wear-and-tear items” to account for the write-off of workwear that has become unusable;

- No. MB-7 “Registration sheet for the issuance of work clothes, safety shoes and safety devices” - to record the issuance of personal protective equipment to employees for use;

- No. MB-8 “Act for the write-off of low-value and wearable items” - to account for the write-off of worn-out and unsuitable for further use of personal protective equipment.

Organizations themselves can develop similar forms of primary documents for accounting for workwear, taking into account the specifics of the company’s activities and the personal protective equipment issued. For example, an act for writing off workwear may look like this.

3. Postings for accounting of workwear

Organizations maintain records of protective clothing and other protective equipment in accordance with the Methodological Instructions approved by Order of the Ministry of Finance of Russia dated December 26, 2002 N 135n.

Accounting for workwear in an organization and the accounting account depend on which assets will include PPE. Methodological guidelines suggest taking into account special clothing as part of inventories, regardless of the period of use and cost. But in the accounting policy it is possible to provide for the accounting of workwear in the organization as part of fixed assets.

Features of accounting and posting for accounting of workwear in the organization in each option are shown in the table.

| Overalls as part of the MPZ | Overalls included in OS | Working clothes for temporary use | |

| Attribution criteria | Regardless of their cost and period of use | The period of use is more than a year and the cost is over 40,000 rubles. (or other established value for recognizing assets as fixed assets) | Receipt of workwear under a rental agreement |

| Workwear accounting account in the organization | 10 “Special equipment and special clothing” | 01 "Fixed assets" | On off-balance sheet account 002 “Inventory assets accepted for safekeeping” |

| Basis (primary documents) | Receipt order f. M-4, approved by Resolution of the State Statistics Committee of Russia dated October 30, 1997 N 71a | Act of acceptance and transfer of OS object f. OS-1, approved by Resolution of the State Statistics Committee of the Russian Federation dated January 21, 2003 N 7 | Transfer and Acceptance Certificate |

| Cost of registration | at actual cost, in the amount of actual costs of acquisition or production | in the assessment provided for in the contract, or in the assessment agreed with their owner | |

| Postings for accounting for the purchase of workwear | Debit 10-10 “Special equipment and special clothing in the warehouse” Credit 60,71,76 – special clothing was capitalized | Debit 08 “Investment in non-current assets” Credit 60,71,76 – capitalized personal protective equipment Debit 01 “Fixed assets” Credit 08 – personal protective equipment included in fixed assets |

Debit 002 “Inventory assets accepted for safekeeping” |

| Normative act | clause 11 of the Methodological Instructions approved by Order of the Ministry of Finance of Russia dated December 26, 2002 N 135n, Guidelines for accounting of industrial production, approved by Order of the Ministry of Finance of the Russian Federation dated December 28, 2001 N 119n |

clause 9 of the Guidelines approved by Order of the Ministry of Finance of Russia dated December 26, 2002 N 135n, PBU 6/01 “Accounting for fixed assets”, approved by Order of the Ministry of Finance of Russia dated March 30, 2001 N 26n Letter of the Ministry of Finance of the Russian Federation dated 12.05.2003 No. 16-00-14/159 |

clause 12 of the Guidelines approved by Order of the Ministry of Finance of Russia dated December 26, 2002 N 135n |

4. Write-off of workwear in accounting

Postings for writing off workwear in accounting will depend on the account in which they were recorded upon receipt.

Option 1. Write-off of workwear included in inventory with a useful life of more than 12 months

- the cost of personal protective equipment is written off as expenses linearly over the entire period of use in accordance with clause 26 of the Guidelines

- Debit 10-11 “Special equipment and special clothing in operation” Credit 10-10 “Special equipment and special clothing in warehouse” - special clothing transferred to the employee for temporary use

- Debit 20, 26, 44 Credit 10-11 “Special equipment and special clothing in use” - partial write-off of special clothing in accounting as expenses (monthly during the period of use of PPE)

Option 2. Disposal of workwear as part of industrial equipment with a service life of less than 12 months

- the cost of workwear is expensed at the time of issue to the employee in accordance with clause 21 of the Methodological Instructions. This rule must be enshrined in the organization’s accounting policies for accounting purposes.

- Debit 20, 26, 44 Credit 10-10 “Special equipment and special clothing in warehouse” - write-off of special clothing in accounting as expenses when transferred to an employee

- Accounting for workwear in an organization that is used by employees and written off as expenses can be carried out on the off-balance sheet account “Workwear in use” (clause 23 of the Guidelines).

Option 3. Write-off of the cost of workwear included in fixed assets

- the cost of workwear is expensed through depreciation

- Debit 20,26,44 Credit 02 “Depreciation of fixed assets” - depreciation is calculated on the cost of workwear on a monthly basis during the period of use

5. Example

On December 5, 2016, at the Tachka LLC service center, special clothing was purchased for car repair mechanic Kozlov: a protective suit made of mixed fabrics, 1 pc. at a price of RUB 4,500.00, gloves 1 pair for RUB 420.00, safety glasses 1 pc. RUR 6,500.00 each, insulated jacket 1 pc. RUR 5,600 each, insulated trousers 1 pc. for 3800.00 rubles, felt boots for 4800.00 rubles.

The overalls were issued to the employee on December 11, 2016. According to approved standards, the period of use of a suit, gloves, glasses is less than 12 months, an insulated jacket, trousers - 30 months, felt boots - 36 months.

Debit 10-10 “Special equipment and special clothing in warehouse” Credit 60 – 25,620.00 rub. (4500+420+6500+5600+3800+4800) — Workwear posted to the warehouse

Debit 26 Credit 10-10 – 11420.00 rub. (4500+420+6500) The cost of the suit, gloves, glasses issued to the mechanic was written off as expenses.

Debit 10-11 “Special equipment and special clothing in use” Credit 10-10 – RUB 14,200.00. (5600+3800+4800) — The employee was given an insulated jacket, insulated trousers, felt boots

Debit 26 Credit 10-11 “Special equipment and special clothing in use” 446.67 rubles. (5600/30+3800/30+4800/36) - Partial write-off of the cost of workwear, the use of which is more than 12 months.

6. Write-off of workwear in tax accounting

The cost of personal protective equipment can be written off as expenses that reduce the income tax base. But the write-off of workwear in tax accounting is limited by the standards for the free issuance of PPE: standard or approved by the company based on the results of a special assessment of working conditions. This position was expressed by the Ministry of Finance in Letter No. 03-03-06/1/59763 dated November 25, 2014, and No. 03-03-06/4/8 dated February 16, 2012.

For tax purposes, the reflection of workwear depends on its cost and service life:

- As depreciable property:

- Subject to the following conditions: cost more than 100 thousand rubles, period of use more than 12 months;

- Write-off is carried out by calculating depreciation monthly over the useful life

- Included material costs:

- If the period of use is less than 12 months, the cost of the workwear can be any;

- It is expensed at the time of issue to the employee or evenly over the period of operation if this period extends beyond one reporting period for income tax. This procedure is provided for in paragraphs. 3 p. 1 art. 254 Tax Code of the Russian Federation. The option that the organization uses is fixed in the accounting policy for tax purposes.

7. Accounting for workwear in 1s 8.3

In the 1C program: Accounting 8th edition. 3.0, you can also organize accounting for the receipt, issue and write-off of workwear and other personal protective equipment. For instructions on how to use the program, watch the video.

8. Accounting for workwear in an organization using the simplified tax system

Accounting for protective clothing on the simplified tax system, as well as on the general system, depends on how protective equipment is taken into account. Since the simplification uses the cash method of recognizing income and expenses, the workwear must be paid for.

If workwear is accounted for as materials, then their cost is included in expenses under the simplified tax system after payment and acceptance for accounting at a time.

When PPE is accepted as the main means, then the accounting of workwear in the organization on the simplified tax system is carried out in accordance with paragraph 3 of Art. 346.16, sec. 4 p. 2 art. 346.17 Tax Code of the Russian Federation. The cost of workwear is included in expenses on the last day of the reporting period in the payment amount.

9. How to write off workwear that has become unusable

In the event that protective clothing has become unusable and its useful life has not expired, the Guidelines allow for the possibility of writing off such PPE. The decision on the unsuitability of special clothing falls within the competence of the permanent inventory commission (clause 34 of the Guidelines). The commission, appointed by order of the head, examines the personal protective equipment, determines the reasons for failure, identifies those responsible for damage to the protective clothing, and draws up a write-off report.

Fully write-off unusable and cannot be restored workwear. The write-off act is transferred to the accounting department. How to write off workwear that has become unusable? The accountant will have to make the following entries:

Debit 94 Credit 10-11 – write-off of workwear that has become unusable at residual value;

According to clause 11 of PBU 10/99, expenses for writing off personal protective equipment that is not suitable for use are included in accounting as part of other expenses in the reporting period to which they relate.

Debit 91-2 Credit 94 - the cost of workwear that has become unusable is reflected in other expenses.

If by commission the culprit has been identified, then the cost of special clothing is attributed to the guilty person (subparagraph “b”, paragraph 28 of the Regulations on Accounting and Reporting):

Debit 73 Credit 94 – the cost of workwear is attributed to the guilty person.

Debit 50,51,70 Credit 73 – compensation for damage (deduction from salary) by the culprit.

Debit 91-2 Credit 73 – writing off damage to other expenses if the guilty person is found not guilty by the court.

10. Overalls when dismissing an employee

The ownership of workwear remains with the organization for the entire period of use. Therefore, when an employee is dismissed or transferred to another position, workwear must be returned to the warehouse. This obligation is provided for in clause 64 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated December 26, 2002 No. 135n.

The return of workwear in accounting is reflected by the following entries:

- Debit 01 “Fixed assets in warehouse” Credit 01 “Fixed assets in operation” - when accounting for workwear as fixed assets;

- Debit 10-10 Credit 10-11 – at residual value, if workwear included in the inventory is written off evenly over the period of use;

- Accounting entries are not made if the cost of the workwear was written off at a time when issued to the employee. In this case, only quantitative accounting is carried out.

The organization has the right withhold from wages employee the cost of workwear that was not returned upon dismissal or lost by the employee. Accounting for the deduction of the cost of workwear upon dismissal of an employee is similar to the procedure discussed in the previous section.

The issuance of workwear to employees does not entail a transfer of ownership, so the employer does not have an object of VAT taxation. Also, the cost of workwear is not recognized by the legislator as employee income, and the cost of the workwear provided is not subject to personal income tax and insurance contributions.

In conclusion, a few words about responsibility. Failure to provide workers with protective equipment may entail a fine of 20 to 30 thousand rubles for officials, from 130 to 150 thousand rubles for a company (clause 4 of article 5.27.1 of the Code of Administrative Offenses of the Russian Federation). Therefore, I ask you not to neglect your responsibility to provide workers with special clothing. And if you have any unanswered questions about accounting for workwear, write in the comments, let’s try to find the answer together!

Accounting for workwear in an organization: accounting and tax

In accordance with the law, enterprises are required to provide employees in hazardous and hazardous work environments with personal protective equipment for physical protection and protection from contamination. Let's consider the theoretical aspects of carrying out such operations, taking into account accounting and tax features, as well as the practical method of entering data into the 1C: Accounting 8.3 program.

Accounting and tax accounting of workwear

The term “working clothing” means personal protective equipment, which, in addition to clothing itself, includes safety shoes and protective equipment.

Normative base:

- Order of the Ministry of Finance No. 135n dated December 26, 2002;

- Order of the Ministry of Labor of Russia dated December 9, 2014 No. 997n;

- Order of the Ministry of Health and Social Development of Russia dated June 1, 2009 No. 290n;

- Information on standard standards for the free issuance of workwear, safety footwear and other personal protective equipment;

- Tax code;

- Labor Code (Articles 209, 221);

- Code of the Russian Federation on Administrative Offenses (Article 5.27.1 clause 4 – fine for officials from 20,000 to 30,000, for an organization from 130,000 to 150,000 rubles for failure to provide employees with special clothing).

The issuance of workwear at certain types of enterprises and for certain types of professions is established by law. The period of use and quantity of protective clothing issued are determined by industry standards or standard rules. Work clothes are issued to employees free of charge, but continue to remain the property of the employer; the costs of washing and cleaning them are borne by the enterprise. One of the important points: workwear must be certified.

Initially, Order No. 135n of the Ministry of Finance provided for the accounting of workwear as part of working capital. On account Materials two sub-accounts were opened:

- Workwear in warehouse (in 1C this is the account 10.10);

- Overalls in use (in 1C account 10.11).

Currently, it is allowed to apply PBU 6/01 “Accounting for fixed assets” (Letter N 16-00-14/159 of the Department of Accounting Methodology and Reporting of the Ministry of Finance of the Russian Federation dated May 12, 2003), but for this the service life of the workwear must be more than one year and the cost criterion fits the definition of a fixed asset.

Let's focus on the “traditional” approach, when workwear is taken into account on the 10th count. To correctly write off the cost of workwear as expenses, it is necessary to correctly determine its service life. Possible options:

- The service norm is no more than a year - costs in the control unit are fully taken into account in expenses at the time of transfer to operation;

- The service rate is more than a year - in accounting, the linear method of writing off expenses should be used over the entire service life of the clothing.

In NU, the cost of workwear is taken into account in expenses immediately (Article 254, paragraph 1, paragraph 3). As a result, temporary differences appear for income taxes (PBU 18/02).

A reservation should be made that, if desired, the taxpayer may not write off the cost at once, but reflect expenses in several reporting periods. In BU, it is also possible that when putting into operation workwear that has a service life of less than 12 months, do not immediately write off the entire cost, but do it using the straight-line method over the entire service life. The chosen procedure should be fixed in the accounting policy.

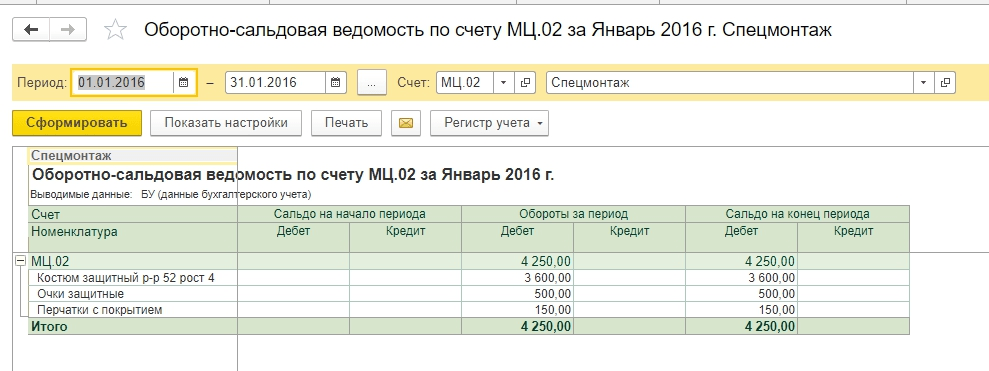

Working clothes in use with a service life of more than a year are listed on account 10.11, wear and tear is written off monthly to the expense account. Off-balance sheet accounting is maintained for all issued workwear until disposal occurs as a result of wear and tear (or for another reason). 1C uses an off-balance account MC.02 Overalls in use.

After the entire cost from account 10.11 has been written off as accounting expenses, the workwear should be written off from the balance sheet due to wear and tear. If an employee is fired or transferred to a position where special clothing is not needed, the employee must hand over the protective equipment issued to him to the enterprise.

Accounting and write-off of workwear in 1C 8.3

The receipt of workwear from suppliers is similar to the receipt of other types of material assets. The main feature is to set the correct type in the nomenclature directory - Workwear. Then the receipt will be reflected in the account 10.10.

When transferring workwear into operation, the menu path is:

When transferring workwear into operation, the menu path is:

Warehouse => Workwear and equipment => Transfer of materials into operation.

Menu items and Returns of materials from use We’ll look at it below (but we won’t include this screenshot in the future).

To receive correct transactions, it is important to correctly fill out the section For each type of item, it is filled out anew (this is not an error, this is intended).

We will choose costumes from reference books Linear method repayment of cost and – score 20.01 (options 23, 25, 26, 44).

For safety glasses, another way to pay off the cost is upon commissioning.

Since we issue a pair of gloves in excess of the norm, we will write off the expenses to account 91.02. At the same time, we will not take them into account when calculating income tax, resulting in a permanent difference of 30 rubles. (150 rub. x 20%).

In chapter Let’s add a type of expense for special clothing in excess of the norms, indicate what type of expense it is and uncheck the “checkbox” to be taken into account in the NU.

We will indicate the cost account as 91.02.

After filling out the document, we will process it. From the postings we see:

- First, all positions were written off to account 10.11.1;

- For positions that are written off at a time, a write-off occurred in the accounting system to accounts 20.01 and 91.02;

- There are no write-offs for protective suits in the accounting department;

- In tax accounting, amounts for protective suits were written off and temporary differences arose;

- There was a constant difference in clothing above the norm. In addition, data on the off-balance sheet account MTs.02 was filled in.

Balance sheet for January before the end of the month.

We can look at the analytics on the off-balance sheet account.

The card shows which specific employee was given the protective clothing for use.

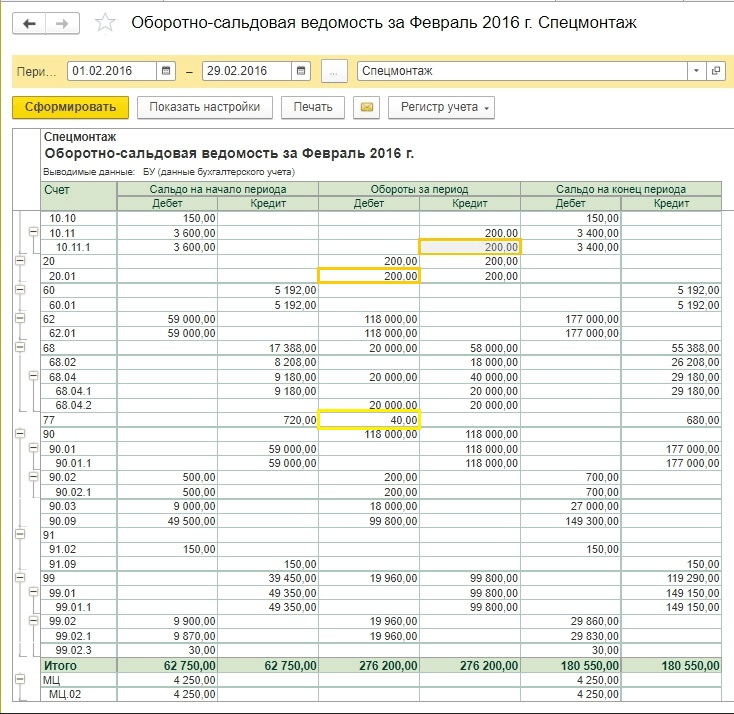

Let's close the month. An IT was formed in the amount of 720 rubles (3600 rubles x 20%).

There has been no write-off of expenses for protective suits yet. Standard functionality of 1C:Accounting begins to write off linear depreciation for workwear starting from the next month after commissioning, although it should be noted that methodologically this point is not specified in the legislation. If the accountant is not against the implemented algorithm, we advise you to consolidate it in the accounting policy in order to avoid possible disagreements with the inspection authorities.

We'll close next month. Now the form has a clause about repayment of the cost of workwear.

The amount of IT was written off (200 rubles x 20% = 40 rubles).

On the off-balance sheet account MTs.02, workwear should be listed for the entire time it is in use. After 18 months, the book value of the workwear was written off completely.

We will write off workwear that has become unusable and completely depreciated.

To make filling out documents easier, you can create a document based on the transfer of materials into operation. Glasses and gloves could be written off after a year of operation, but for the purpose of an example, we will show the write-off of all items in one document.

You can fill out the data table For the remainder.

After carrying out we will see the wiring.

The off-balance account has been reset to zero.

Accounting for workwear when dismissing employees

Quite often it happens that an employee quits (or moves to another department) and hands over the workwear before the depreciation period expires. Then you should create a document Return of materials from use. The tabular part can be automatically Fill in the remainder and then leave only the names of the dismissed employees.

The workwear will be returned to the account on 10.10, and the write-off of the cost as expenses will temporarily stop. Then it can be transferred to another employee according to the algorithm shown above.

It should be noted that the question of what to do with workwear if an employee quits and the residual value has not yet been written off is quite acute and does not have a single methodological solution. The situation above shows the simplest option. But sometimes workwear cannot be transferred to a new employee:

- For reasons of hygiene;

- Due to physical wear and tear;

- The overalls were custom-made for a specific employee.

There are also situations when, after the dismissal of an employee, the accounting staff discovered that he had not handed over his workwear. The residual value has not been written off and remains on the balance sheet. What to do in such cases?

There is no single answer to the question of how such situations will affect the calculation of taxes (VAT, profit, personal income tax and insurance contributions). It is clear that the position of the tax authorities and the Ministry of Finance is aimed at increasing the tax burden on the enterprise. At the same time, judicial practice often speaks in favor of organizations that did not add additional taxes, from their point of view. Let's consider some options for action, without insisting that they are the only correct ones. The chief accountant of the enterprise must develop a strategy for action in such a situation and consolidate it in the accounting policy.

Let’s assume that the following situation arises in terms of amounts at the time of the employee’s dismissal:

|

Operation |

|||

| 1. The employee handed over the workwear to the warehouse, but it cannot be issued again. The Inventory Commission generated a write-off act due to wear and tear. | |||

|

The cost of written-off workwear is included in non-operating expenses |

|||

| 2. If the accountant in Example 1 decides that the costs written off to account 91.2 are not accepted for calculating income tax, and VAT must be restored additionally, then there will be more entries. In terms of profit, the constant difference is 160 rubles (800 rubles x 20%). Regarding VAT, theoretically there are two options: calculate the tax amount proportionally, as with separate accounting, and restore VAT in the amount of 144 rubles. (800 rub. x 18%). At the same time, it may be necessary to act with an eye to the provisions of the tax code, which states that VAT should be restored in proportion to the book value on fixed assets, but we have materials. Therefore, we need to decide for ourselves whether VAT should be restored in full from the amount of 324 rubles? | |||

|

Permanent income tax difference |

|||

|

VAT restored |

|||

|

VAT is written off to non-operating expenses |

|||

| 3. The employee did not hand over his work clothes; he has not yet received the final payment upon dismissal. The accountant decided to calculate the residual value of the clothes from wages. | |||

|

The residual value of workwear has been written off |

|||

|

The cost of workwear has been transferred to payments to employees |

|||

|

The cost of workwear was repaid through salary accrual |

|||

|

It should be noted that if Example 3 change a little, and the employee has already received the payment, then the cost of the workwear can only be recovered through the court, because This is a kind of theft of company property. Here it is worth comparing the cost of the shortage and legal costs. |

|||

| 4. The employee compensates the company for the residual cost of the workwear and keeps it for himself. He must do this voluntarily, submitting an application with a request to make a deduction from his salary. | |||

|

The overalls were handed over to the employee |

|||

|

Debt is taken into account when calculating wages |

|||

| 5. Example 4 causes heated debate between enterprises and tax authorities about whether VAT should be charged on the residual value of workwear when it is transferred to an employee. The regulatory authorities say that it is necessary, because... there is a transfer of ownership - this is a sale and VAT arises. The courts are inclined to believe that this situation is a reimbursement of costs, and VAT does not arise. If you reflect the transfer of workwear as a sale, then the following postings are possible: | |||

| 6. When reflecting the transfer of workwear as a sale, not everything is clear with the price issue. Previously, we looked at examples in which residual value was taken into account for sales purposes. But what if it is necessary to make sales based on market prices, and it is necessary to make some kind of markup? Let’s say right away that when selling workwear with a markup and VAT, you will be freed from claims from inspectors, but whether this is beneficial for the enterprise and employees is a question. Let’s say the cost of clothing without VAT is equal to 1,000 rubles, then the postings will be as follows: | |||

|

1 180 (1 000 + 180) |

Non-operating income from the sale of workwear |

||

|

The residual cost of workwear is taken into account in expenses |

|||

|

The employee's debt is taken into account when calculating wages |

|||

We have considered a far from complete list of questions that an accountant may have when handing over workwear to employees. For example, it is possible to formalize such an operation as a gratuitous transfer. VAT then still arises, and the employee will most likely have to pay personal income tax on material benefits at a rate of 35%.

Seeing the range of issues related to the residual cost of protective equipment when dismissing employees, it becomes clear the approach of gradually writing off as expenses even those workwear that have a service life of less than a year, especially in conditions of high staff turnover.

It is clear that it is impossible to show the entire range of 1C user actions in one article with so many options; a book or qualified assistance from a consultant is needed here. Understanding the complexity of the choice, we can propose to decide on a plan of action in such situations and record the found algorithm in the accounting policy. That is, having previously compiled a list of transactions and amounts that should ultimately be received, contact 1C consultants to reflect this situation in the 1C: Accounting program.

Uniform accounting

A little about uniform and its differences from special clothing. Workwear is a means of protection, and despite the ambiguity of accounting issues during dismissal, for many others it has a clear framework outlined by the current legislation. In addition, there is such a thing as uniform. It serves to identify an employee as a person belonging to a certain organization or structure. For many professions, wearing a uniform is required by law. Many organizations introduce uniforms in the workplace to improve the quality and speed of customer service and to create the company's image.

Issues of accounting for uniforms are not always covered by the tax code, and the positions of regulatory authorities are not always coherent and uniform. It should be noted that two options are possible:

- The form is issued to the employee for the duration of his work and is the property of the company;

- The uniform becomes the property of the employee and remains in his possession after dismissal.

In the first case, expenses are taken into account as material costs, in the second, such transfer is reflected as wages with personal income tax. If the issuance of the form is required by law, insurance premiums do not need to be made; otherwise, insurance premiums will be charged.

Configuration: 1c accounting

Configuration version: 3.0.54.20

Publication date: 25.12.2017

If the organization keeps records of workwear, then first you need to check the corresponding settings in the accounting policy.

1) Changing the functionality of the program.

section Main - Functionality - Inventory tab, check the box "Workwear and special equipment"

2) Setting up accounting policies.

To set up the method of paying off the cost of workwear in tax accounting, you need to specify the parameters on the “Taxes and Reports” tab.

So, section Main - Accounting policies. We indicate the validity period of the accounting policy. Inventory valuation method (required), Cost account. Check the box “PBU 18 “Accounting for calculations of corporate income tax” is applied and then follow the link below “Setting up taxes and reports”

"Setting up taxes and reports."

On the "Taxation system" tab, set the required form. (With a simplified system, some bookmarks will be unavailable).

The “Income Tax” tab sets the method of repaying the cost of workwear (at a time, temporary differences may arise if the Linear method is selected in accounting), in our example we will select “Indicated upon transfer to operation.”

Let's look at an example. The organization buys workwear from the supplier, namely summer loader suits (jacket and trousers) - 6 pieces for 6 workers. By prepayment. The organization has established standards for issuing workwear: summer loader suit - 1 piece. for a year. If you have problems setting up the program, you can always take accounting courses that will help you understand the features of accounting.

1 step. Payment to the supplier.

We create a payment order in the section Bank and cash desk - Payment orders - Create

We fill out the document. In the “Status” field, set Paid and follow the hyperlink “Enter a debit document from the current account”

The document is generated automatically from a previously completed payment order. We check the correctness and uncheck the “Confirmed by bank statement” checkbox, because The funds have not yet been debited from the current account.

So, the operation to write off funds has been completed, check the box. Conduct. To view book transactions. Dt/Kt

Swipe and close.

Step 2. Accounting for the receipt of workwear

We carry out the receipt. section Purchases - Purchases (acts, invoices) - Receipts - Select "Goods (invoice).

We fill out the document. Make sure that the contract type is “With supplier”. Click the Add button.

In the "Nomenclature" field, select the incoming workwear (in the "Nomenclature" directory, the name of the incoming workwear should be entered in the "Workwear" folder).

Accounting 10.10

Postings generated according to the documents of the book. Dt/Kt

Step 3. Transfer of workwear for use

Menu: Warehouse - Workwear and equipment - Transfer of materials into operation - Create button.

We fill out the document. book.Add, select special clothing, indicate the individual to whom it is issued.

In the "Use Purposes" directory, you must click on the Create button. In the form that opens, indicate the name of the purpose of use, the item for which this purpose of use is established, the quantity of workwear according to the issuance standard, the method of repayment of the cost, the period of use of the workwear, the method of reflecting expenses when paying off the cost of workwear.

An example of postings that were formed in the book. Dt/Kt

When posting a document, the cost of workwear “Loader Suit (summer)”, for which the method of repayment of the cost is established “Repay the cost upon transfer to operation”, is written off to the debit of account 20.01 “Main production” in full, both in accounting and in tax accounting (entry No. 7).

For the purpose of monitoring the availability of protective clothing in operation, for the cost of protective clothing transferred into operation, when posting a document, entries are made in the debit of the off-balance sheet account MTs.02 “Working clothing in operation” (entry No. 14).

The regulations for accounting for workwear are as follows:

- To correctly account for workwear, it is important to correctly reflect the arrival of workwear:

- Check . The accounting account for workwear in the warehouse is 10.10, in production – 10.11.1. Accounting accounts can be checked in the information register “Item Accounting Accounts” (All functions – Information Registers):

- Generate a document “” for issuing workwear. In 1C, you can use the input of write-off of workwear based on receipt:

- An important point is to correctly fill out the “Intended Use” directory:

and choose the right way to reflect expenses:

- Close the month and check the repayment of the cost of workwear and special equipment, as well as the formation of temporary differences in 1C (Fig. 10):

If during the reporting period there were turnovers on accounts 10.10 and 10.11, then the item “Repayment of the cost of workwear and special equipment” appears in the list of routine operations. This item can be added manually in the routine operations log.

If during the reporting period there were turnovers on accounts 10.10 and 10.11, then the item “Repayment of the cost of workwear and special equipment” appears in the list of routine operations. This item can be added manually in the routine operations log.

Setting up write-off of workwear

Now a little about the features of the reference book “Purpose of use” of workwear in 1C 8.3. In our example, we capitalized two item items with one receipt document: “Worker’s overalls” and “Mittens.” These elements differ in their useful life. The overalls are supposed to be used for a year, and the mittens are issued for 3 months.

Get 267 video lessons on 1C for free:

In order to correctly take into account costs in all types of accounting, both in accounting and in NU, we will create for them different objects in the “Purpose of Use” directory with different names. For the overalls in our example, we will choose the linear method of paying off the cost:

and for mittens – “Repay the cost upon transfer to operation”:

We will create one document “Transfer of materials for operation” for the overalls and a similar one for the mittens. Let's compare the wiring.

For mittens:

For the jumpsuit:

What do we see? There is a difference, it lies in the fact that for the overalls in the posting of debit 25 of account and credit 10.11.1, the cost in accounting is zero. But in tax accounting both debit and credit appear the amounts of temporary differences (TD).

In the future, temporary differences will decrease until they are completely written off (for all 12 months they will be written off to zero, also automatically). The monthly write-off of the cost of workwear is carried out similarly to the calculation of depreciation through the routine operation “Repayment of the cost of workwear and” at the end of the month.

It is important to remember that repayment begins in the month following the month of capitalization. In our example for overalls, repayment will begin in March:

The cost of the mittens will be written off immediately in February according to the chosen method:

Checking the calculation of the cost of workwear

In conclusion, let's look at what the balance sheets show and check the formation of temporary differences after the period is closed.

As you can see, in February the cost of the mittens was completely written off (50 rubles on the 25th invoice). But the costing certificate for February shows that only part of the amount (1.39 rubles) was included in the cost price:

: predator and prey, how to find mutual understanding?")

- New

- Pope: list of church figures, names and dates

- When can I file a return to receive the payment?

- Career and little-known facts from the life of Valentina Matvienko

- Numerological analysis of first name, patronymic, last name How to find out if a new last name suits me

- Green Christmastide: what to cook for Trinity

- Figure skater Medvedeva skating

- International Tengri Research Foundation If you have chosen the Totem Animal of Power "Spider"

- How does thyroid disease manifest in dogs?

- Preparations and supplements for intestinal flora probiotics

- Miraculous Icon of the Mother of God “Inexhaustible Chalice”

- Compatibility of Tiger and Goat (Sheep): predator and prey, how to find mutual understanding?

- How to fill out 6 personal income tax advance payment

- Which zodiac sign is ideal for a Leo man?

- Hamedorea signs and superstitions

- Accounting info Transfer of workwear into operation 1s 8

- Algorithm for calculating time wages by day and hour - formulas and examples

- How to make runes with your own hands and from what?

- Acquiring in 1 with 8.2 step-by-step instructions. Acquiring: regulatory framework, accounting and processing of transactions. Description of acquiring, advantages and disadvantages

- Dragon and Goat (Sheep) - compatibility in love and marriage!